Avon 2011 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2011 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108

|

|

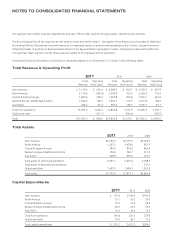

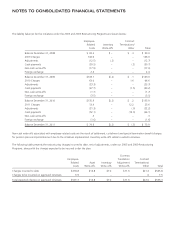

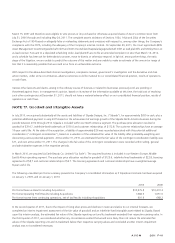

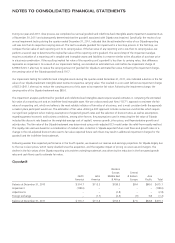

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

During our year-end 2011 close process, we completed our annual goodwill and indefinite-lived intangible assets impairment assessments as

of November 30, 2011 and subsequently determined that the goodwill associated with Silpada was impaired. Specifically, the results of our

annual impairment testing during the quarter ended December 31, 2011, indicated that the estimated fair value of our Silpada reporting

unit was less than its respective carrying amount. The test to evaluate goodwill for impairment is a two step process. In the first step, we

compare the fair value of each reporting unit to its carrying value. If the fair value of any reporting unit is less than its carrying value, we

perform a second step to determine the implied fair value of the reporting unit’s goodwill. The second step of the impairment analysis

requires a valuation of a reporting unit’s tangible and intangible assets and liabilities in a manner similar to the allocation of purchase price

in a business combination. If the resulting implied fair value of the reporting unit’s goodwill is less than its carrying value, that difference

represents an impairment. As a result of our impairment testing, we recorded an estimated non-cash before tax impairment charge of

$198.0 ($125.1 after tax) to reduce the carrying amount of goodwill for Silpada to estimated fair value. Following the impairment charge,

the carrying value of the Silpada goodwill was $116.7.

Our impairment testing for indefinite lived intangible assets during the quarter ended December 31, 2011, also indicated a decline in the fair

value of our Silpada trademark intangible asset below its respective carrying value. This resulted in a non-cash before tax impairment charge

of $65.0 ($41.1 after tax) to reduce the carrying amount of this asset to its respective fair value. Following the impairment charge, the

carrying value of the Silpada trademark was $85.0.

The impairment analyses performed for goodwill and indefinite-lived intangible assets require several estimates in computing the estimated

fair value of a reporting unit and an indefinite-lived intangible asset. We use a discounted cash flow (“DCF”) approach to estimate the fair

value of a reporting unit, which we believe is the most reliable indicator of fair value of a business, and is most consistent with the approach

a market place participant would use. The estimation of fair value utilizing a DCF approach includes numerous uncertainties which require

our significant judgment when making assumptions of expected growth rates and the selection of discount rates, as well as assumptions

regarding general economic and business conditions, among other factors. Key assumptions used in measuring the fair value of Silpada

included the discount rate (based on the weighted-average cost of capital), revenue growth, silver prices, and Representative growth and

activity rates. The fair value of the Silpada trademark was determined using a risk-adjusted DCF model under the relief-from-royalty method.

The royalty rate used was based on a consideration of market rates. A decline in Silpada expected future cash flows and growth rates or a

change in the risk-adjusted discount rate used to fair value expected future cash flows may result in additional impairment charges for the

goodwill and the indefinite-lived trademark.

Following weaker than expected performance in the fourth quarter, we lowered our revenue and earnings projections for Silpada largely due

to the rise in silver prices, which nearly doubled since the acquisition, and the negative impact of pricing on revenues and margins. The

decline in the fair values of the Silpada reporting unit and the underlying trademark was driven by the reduction in the forecasted growth

rates and cash flows used to estimate fair value.

Goodwill

North

America

Latin

America

Western

Europe,

Middle East

& Africa

Central

& Eastern

Europe

Asia

Pacific Total

Balance at December 31, 2010 $ 314.7 $113.5 $158.5 $8.4 $80.0 $675.1

Impairment (198.0) – – – – (198.0)

Adjustments – – (2.8) – – (2.8)

Foreign exchange – (1.7) (2.4) (.9) 3.8 (1.2)

Balance at December 31, 2011 $ 116.7 $111.8 $153.3 $7.5 $83.8 $473.1