Foot Locker 2008 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2008 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

58

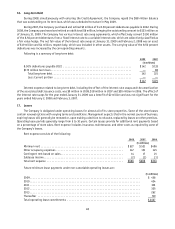

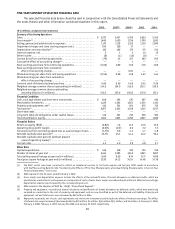

The following tables set forth the changes in accumulated other comprehensive loss (pre-tax) at January 31, 2009:

Pension

Benefits

Postretirement

Benefits

(in millions)

Net actuarial loss (gain) at beginning of year .................. $305 $(47)

Amortization of net (loss) gain ............................. (11) 8

Loss (gain) arising during the year .......................... 164 (2)

Translation loss. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (10) —

Net actuarial loss (gain) at end of year ....................... $448 $(41)

Net prior service cost (benefit) at beginning of year ............. $ 3 $ (6)

Amortization of prior service (cost) benefit ................... (1) 3

Net prior service cost (benefit) at end of year .................. $ 2 $ (3)

Total amount recognized .................................. $450 $(44)

The amounts in accumulated other comprehensive loss that are expected to be recognized as components of net

periodic benefit cost (income) during the next year are as follows:

Pension

Postretirement

Benefits Total

(in millions)

Amortization of prior service cost (benefit) ................... $ 1 $— $1

Amortization of net loss (gain) ............................. $13 $(7) $6

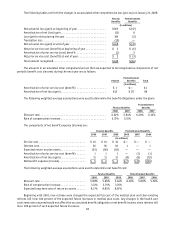

The following weighted-average assumptions were used to determine the benefit obligations under the plans:

Pension Benefits

Postretirement

Benefits

2008 2007 2008 2007

Discount rate .......................................... 6.22% 5.84% 6.20% 6.10%

Rate of compensation increase ............................. 3.72% 3.72%

The components of net benefit expense (income) are:

Pension Benefits Postretirement Benefits

2008 2007 2006 2008 2007 2006

(in millions)

Service cost .............................. $ 10 $ 10 $ 10 $— $— $—

Interest cost .............................. 36 36 36 1 — 1

Expected return on plan assets ................ (53) (56) (56) — — —

Amortization of prior service cost (benefit) ...... 1 1 1 — (1) (1)

Amortization of net loss (gain) ................ 11 11 12 (8) (8) (10)

Net benefit expense (income) ................. $ 5 $ 2 $ 3 $(7) $(9) $(10)

The following weighted-average assumptions were used to determine net benefit cost:

Pension Benefits Postretirement Benefits

2008 2007 2006 2008 2007 2006

Discount rate ............................. 5.88% 5.66% 5.44% 6.10% 5.80% 5.50%

Rate of compensation increase ................ 3.72% 3.75% 3.76%

Expected long-term rate of return on assets ...... 8.17% 8.85% 8.87%

Beginning with 2001, new retirees were charged the expected full cost of the medical plan and then-existing

retirees will incur 100 percent of the expected future increases in medical plan costs. Any changes in the health care

cost trend rates assumed would not affect the accumulated benefit obligation or net benefit income, since retirees will

incur 100 percent of such expected future increases.