Foot Locker 2008 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2008 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

57

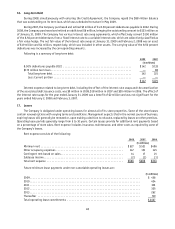

24. Retirement Plans and Other Benefits

Pension and Other Postretirement Plans

The Company has defined benefit pension plans covering most of its North American employees, which are

funded in accordance with the provisions of the laws where the plans are in effect. In addition to providing pension

benefits, the Company sponsors postretirement medical and life insurance plans, which are available to most of its

retired U.S. employees. These plans are contributory and are not funded. The measurement date of the assets and

liabilities is the last day of the fiscal year.

In September 2006, the FASB issued SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension and

Other Postretirement Plans- An Amendment of FASB Statements No. 87, 88, 106, and 132(R),” (“SFAS No. 158”). This

standard requires an employer to: recognize in its statement of financial position an asset for a plan’s overfunded

status or a liability for a plan’s underfunded status; measure a plan’s assets and its obligations that determine its

funded status as of the end of the employer’s fiscal year (with limited exceptions); and recognize changes in the

funded status of a defined benefit postretirement plan in the year in which the changes occur. Those changes will be

reported in accumulated comprehensive loss. The initial effect of the standard, due to unrecognized prior service cost

and net actuarial gains or losses, as well as subsequent changes in the funded status, is recognized as a component

of accumulated comprehensive income/loss within shareholders’ equity. Additional minimum pension liabilities and

related intangible assets are derecognized upon the adoption of SFAS No. 158. The Company adopted this standard as

of February 3, 2007.

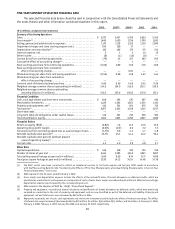

The following tables set forth the plans’ changes in benefit obligations and plan assets, funded status and

amounts recognized in the Consolidated Balance Sheets, measured at January 31, 2009 and February 2, 2008:

Pension Benefits

Postretirement

Benefits

2008 2007 2008 2007

(in millions)

Change in benefit obligation

Benefit obligation at beginning of year.................... $ 649 $662 $ 10 $ 13

Service cost ........................................ 10 10 — —

Interest cost........................................ 36 36 1 —

Plan participants’ contributions ......................... — — 4 4

Actuarial gain ...................................... (15) (13) (2) (2)

Foreign currency translation adjustments .................. (18) 15 — —

Plan amendment..................................... — — 3 —

Benefits paid ....................................... (58) (61) (4) (5)

Benefit obligation at end of year ........................ $ 604 $649 $ 12 $ 10

Change in plan assets

Fair value of plan assets at beginning of year ............... $ 611 $647

Actual return on plan assets ............................ (127) 9

Employer contribution ................................ 8 2

Foreign currency translation adjustments .................. (16) 14

Benefits paid ....................................... (58) (61)

Fair value of plan assets at end of year .................... $ 418 $611

Funded status ....................................... $(186) $(38) $(12) $(10)

Balance Sheet caption reported in:

Accrued and other liabilities............................ (3) (3) (1) (1)

Other liabilities ..................................... (183) (35) (11) (9)

$(186) $ (38) $(12) $(10)

At January 31, 2009 and February 2, 2008, the aggregate amount of accumulated benefit obligations, which

exceed plan assets, totaled $603 million and $648 million, respectively, representing both the qualified and non

qualified pension plans.