Chevron 2005 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2005 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

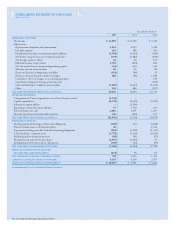

CHEVRON CORPORATION 2005 ANNUAL REPORT 49

NEW ACCOUNTING STANDARDS

FASB Statement No. 151, “Inventory Costs, an Amendment of

ARB No. 43, Chapter 4” (FAS 151) In November 2004, the

FASB issued FAS 151, which became effective for the com-

pany on January 1, 2006. The standard amends the guidance

in Accounting Research Bulletin (ARB) No. 43, Chapter 4,

“Inventory Pricing” to clarify the accounting for abnormal

amounts of idle facility expense, freight, handling costs and

spoilage. In addition, the standard requires that allocation

of fi xed production overheads to the costs of conversion be

based on the normal capacity of the production facilities.

The adoption of this standard will not have an impact on the

company’s results of operations, fi nancial position or liquidity.

EITF Issue No. 04-6, “Accounting for Stripping Costs

Incurred during Production in the Mining Industry” (Issue

04-6) In March 2005, the FASB ratifi ed the earlier EITF

consensus on Issue 04-6, which became effective for the

company on January 1, 2006. Stripping costs are costs of

removing overburden and other waste materials to access

mineral deposits. The consensus calls for stripping costs

incurred once a mine goes into production to be treated

as variable production costs that should be considered a

component of mineral inventory cost subject to ARB No.

43, “Restatement and Revision of Accounting Research

Bulletins.” Adoption of this accounting for its coal, oil sands

and other mining operations will not have a signifi cant effect

on the company’s results of operations, fi nancial position or

liquidity.