US Cellular 2009 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2009 US Cellular annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

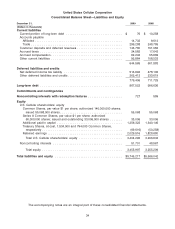

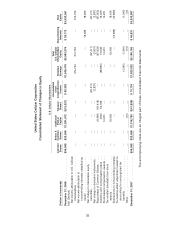

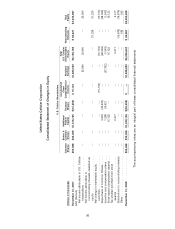

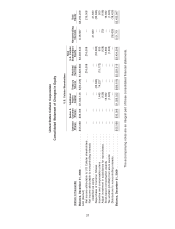

UNITED STATES CELLULAR CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND RECENT ACCOUNTING

PRONOUNCEMENTS

United States Cellular Corporation (‘‘U.S. Cellular’’), a Delaware Corporation, is an 82%-owned subsidiary

of Telephone and Data Systems, Inc. (‘‘TDS’’).

Nature of Operations

U.S. Cellular owns, operates and invests in wireless systems throughout the United States. As of

December 31, 2009, U.S. Cellular served 6.1 million customers in 26 states, representing a total

population in its operating markets of approximately 46.3 million. U.S. Cellular operates as one

reportable segment.

Principles of Consolidation

The accounting policies of U.S. Cellular conform to accounting principles generally accepted in the

United States of America (‘‘GAAP’’) as set forth in the Financial Accounting Standards Board (‘‘FASB’’)

Accounting Standards Codification (‘‘ASC’’). Unless otherwise specified, references to accounting

provisions and GAAP in these notes refer to the requirements of the FASB ASC. The consolidated

financial statements include the accounts of U.S. Cellular, its majority-owned subsidiaries, general

partnerships in which U.S. Cellular has a majority partnership interest and any entity in which

U.S. Cellular has a variable interest that requires U.S. Cellular to recognize a majority of the entity’s

expected gains or losses. All material intercompany accounts and transactions have been eliminated.

Reclassifications

Certain prior year amounts have been reclassified to conform to the 2009 financial statement

presentation. These reclassifications did not affect consolidated net income attributable to U.S. Cellular

shareholders, cash flows, assets, liabilities or equity for the years presented.

Business Combinations Accounting

Effective January 1, 2009, U.S. Cellular adopted new required provisions under GAAP related to

accounting for business combinations. Although the revised provisions still require that all business

combinations are to be accounted for at fair value in accordance with the acquisition method, they

require U.S. Cellular to revise its application of the acquisition method in a number of significant aspects.

Specifically, the new provisions require that transaction costs are to be expensed and that the acquirer

must recognize 100% of the acquiree’s assets and liabilities rather than a proportional share, for

acquisitions of less than 100% of a business. In addition, the revised provisions eliminate the step

acquisition model and provide that all business combinations, whether full, partial or step acquisitions,

will result in all assets and liabilities of an acquired business being recorded at their fair values at the

acquisition date.

During 2008 and 2007, U.S. Cellular applied the provisions of GAAP related to business combinations in

effect during those periods. Similar to the revised provisions, the previous provisions required the

application of the acquisition method whereby business combinations were to be accounted for at fair

value. However, the previous provisions were different in a number of respects, including (but not limited

to) the requirement that all direct and incremental costs relating to an acquisition be included in the

acquisition costs, and the requirement that the acquirer only recognize its proportional share of the fair

value of assets and liabilities acquired in a partial business acquisition.

39