U-Haul 2007 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2007 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

In February 2004, SAC Holding Corporation restructured the indebtedness of three subsidiaries and then

distributed its interest in those subsidiaries to its sole shareholder. This triggered a requirement to reassess

AMERCO’ s involvement with those subsidiaries, which led to the conclusion that based on current contractual and

ownership interests between

20

AMERCO and this entity, AMERCO ceased to have a variable interest in those three

su

’ s ability to fund its own operations and execute its business

pl

nt

an

ccur, we could be required to consolidate some or all of SAC Holding Corporation with

ou

be required to deconsolidate some or all of our variable interest in SAC Holding II

R

preciation rate, historical disposal experience, holding periods and

tr

iginally estimated, the net book value of the assets is depreciated over the newly determined

re

toric cost. The adjustment reflects management’ s best estimate of the estimated residual

value of the rental trucks.

bsidiaries at that date.

Separately, in March 2004, SAC Holding Corporation restructured its indebtedness, triggering a similar

reassessment of SAC Holding Corporation that led to the conclusion that SAC Holding Corporation was not a VIE

and that AMERCO ceased to be the primary beneficiary of SAC Holding Corporation and its remaining subsidiaries.

This conclusion was based on SAC Holding Corporation

an without any future subordinated financial support.

Accordingly, at the dates AMERCO ceased to have a variable interest and ceased to be the primary beneficiary of

SAC Holding Corporation and its current or former subsidiaries, it deconsolidated those entities. The

deconsolidation was accounted for as a distribution of SAC Holding Corporations interests to the sole shareholder of

the SAC entities. Because of AMERCO’ s continuing involvement with SAC Holding Corporation and its curre

d former subsidiaries, the distributions do not qualify as discontinued operations as defined by SFAS No. 144.

It is possible that SAC Holding Corporation could take actions that would require us to re-determine whether SAC

Holding Corporation has become a VIE or whether we have become the primary beneficiary of SAC Holding

Corporation. Should this o

r financial statements.

Similarly, SAC Holding II could take actions that would require us to re-determine whether it is a VIE or whether

we continue to be the primary beneficiary of our variable interest in SAC Holding II. Should we cease to be the

primary beneficiary, we would

from our financial statements.

ecoverability of Property, Plant and Equipment

Property, plant and equipment are stated at cost. Interest expense incurred during the initial construction of

buildings and rental equipment is considered part of cost. Depreciation is computed for financial reporting purposes

using the straight-line or an accelerated method based on a declining balance formula over the following estimated

useful lives: rental equipment 2-20 years and buildings and non-rental equipment 3-55 years. The Company follows

the deferral method of accounting based in the AICPA’ s Airline Guide for major overhauls in which engine

overhauls are capitalized and amortized over five years and transmission overhauls are capitalized and amortized

over three years. Routine maintenance costs are charged to operating expense as they are incurred. Gains and losses

on dispositions of property, plant and equipment are netted against depreciation expense when realized. Equipment

depreciation is recognized in amounts expected to result in the recovery of estimated residual values upon disposal,

i.e., no gains or losses. In determining the de

ends in the market for vehicles are reviewed.

We regularly perform reviews to determine whether facts and circumstances exist which indicate that the carrying

amount of assets, including estimates of residual value, may not be recoverable or that the useful life of assets is

shorter or longer than originally estimated. Reductions in residual values (i.e., the price at which we ultimately

expect to dispose of revenue earning equipment) or useful lives will result in an increase in depreciation expense

over the life of the equipment. Reviews are performed based on vehicle class, generally subcategories of trucks and

trailers. We assess the recoverability of our assets by comparing the projected undiscounted net cash flows

associated with the related asset or group of assets over their estimated remaining lives against their respective

carrying amounts. We consider factors such as current and expected future market price trends on used vehicles and

the expected life of vehicles included in the fleet. Impairment, if any, is based on the excess of the carrying amount

over the fair value of those assets. If asset residual values are determined to be recoverable, but the useful lives are

shorter or longer than or

maining useful lives.

During the fourth quarter of fiscal 2007, based on economic market analysis, the Company decreased the

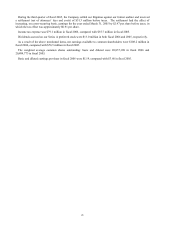

estimated residual value of certain rental trucks. The effect of the change decreased pre-tax earnings for fiscal 2007

by $2.0 million. The in-house analysis of truck sales compared such factors as the truck model, size, age and average

residual value of units sold. Based on the analysis, the estimated residual values of these vehicles were decreased to

approximately 20% of his