U-Haul 2007 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2007 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

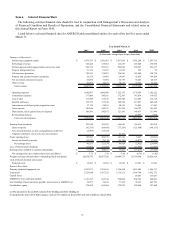

Net revenue from our SAC Holding II operating segment wa

6

s approximately 1.3%, 1.3% and 1.1% of

net revenue in fiscal 2007, 2006 and 2005, respectively.

E

merica with approximately

s working within our Moving and Storage operating segment.

Sa

ndependent U-Haul dealers through advertising of U-Haul moving and self-storage

re

to our retail centers through independent U-Haul dealers, and by

ex

y 30% of the reservations made for U-Move rentals were completed through the Company’ s website.

M

e. Our major

co

mpetitors in the

rage Inc., Extra Space Storage, Inc., and Sovran Self-Storage Inc.

In

pete in the insurance

business based upon price, product design, and services rendered to agents and policyholders.

consolidated

mployees

As of March 31, 2007, we employed approximately 18,000 people throughout North A

98% of these employee

les and Marketing

We promote U-Haul brand awareness through direct and co-marketing arrangements. Our direct marketing

activities consist of yellow pages, print and web based advertising as well as trade events, movie cameos of our

rental fleet and boxes, and industry and consumer communications. Our rental equipment is our best form of

advertisement. We support our i

ntals, products and services.

Our marketing plan includes maintaining our leadership position with U-Haul being synonymous with “do-it-

yourself” moving and storage. We accomplish this by continually improving the ease of use and efficiency of our

rental equipment, by providing added convenience

panding the capabilities of our eMove web site.

A significant driver of U-Haul’ s rental transaction volume is our utilization of an online reservation and sales

system, through www.uhaul.com, www.eMove.com and our 24-hour 1-800-GO-U-HAUL telephone reservations

system. The Company’ s 1-800-GO-U-HAUL telephone reservation line is prominently featured on nationwide

yellow page advertising, its websites and on the outside of its vehicles, and is a major driver of customer lead

sources. Nearl

Competition

oving and Storage Operating Segment

The moving truck and trailer rental industry is large and highly competitive. There are two distinct users of rental

trucks: commercial and “do-it-yourself” residential users. We focus primarily on the “do-it-yourself” residential

user. Within this segment, we believe the principal competitive factors are convenience of rental locations,

availability of quality rental moving equipment, breadth of essential products and services, and pric

mpetitors in the moving equipment rental market are AvisBudget Group and Penske Truck Leasing.

The self-storage market is large and highly fragmented. We believe the principal competitive factors in this

industry are convenience of storage rental locations, cleanliness, security and price. Our primary co

self-storage market are Public Sto

surance Operating Segments

The highly competitive insurance industry includes a large number of life insurance companies and property and

casualty insurance companies. In addition, the marketplace includes financial services firms offering both insurance

and financial products. Some of the insurance companies are owned by stockholders and others are owned by

policyholders. Many competitors have been in business for a longer period of time or possess substantially greater

financial resources and broader product portfolios than our insurance companies. We com