Tyson Foods 2009 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2009 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

37

Commodities Risk: We purchase certain commodities, such as grains and livestock, in the course of normal operations. As part of

our commodity risk management activities, we use derivative financial instruments, primarily futures and options, to reduce the effect

of changing prices and as a mechanism to procure the underlying commodity. However, as the commodities underlying our derivative

financial instruments can experience significant price fluctuations, any requirement to mark-to-market the positions that have not

been designated or do not qualify as hedges could result in volatility in our results of operations. Contract terms of a hedge instrument

closely mirror those of the hedged item providing a high degree of risk reduction and correlation. Contracts designated and highly

effective at meeting this risk reduction and correlation criteria are recorded using hedge accounting. The following table presents a

sensitivity analysis resulting from a hypothetical change of 10% in market prices as of October 3, 2009, and September 27, 2008, on

the fair value of open positions. The fair value of such positions is a summation of the fair values calculated for each commodity by

valuing each net position at quoted futures prices. The market risk exposure analysis includes hedge and non-hedge derivative

financial instruments.

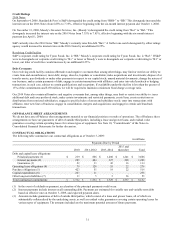

Effect of 10% change in fair value

in millions

2009

2008

Livestock:

Cattle

$

20

$

78

Hogs

12

31

Grain

1

88

Interest Rate Risk: At October 3, 2009, we had fixed-rate debt of $3.3 billion with a weighted average interest rate of 7.9%. We

have exposure to changes in interest rates on this fixed-rate debt. Market risk for fixed-rate debt is estimated as the potential increase

in fair value, resulting from a hypothetical 10% decrease in interest rates. A hypothetical 10% decrease in interest rates would have

increased the fair value of our fixed-rate debt by approximately $32 million at October 3, 2009, and $45 million at September 27,

2008. The fair values of our debt were estimated based on quoted market prices and/or published interest rates.

At October 3, 2009, we had variable rate debt of $218 million with a weighted average interest rate of 4.3%. A hypothetical 10%

increase in interest rates effective at October 3, 2009, and September 27, 2008, would have a minimal effect on interest expense.

Foreign Currency Risk: We have foreign exchange gain/loss exposure from fluctuations in foreign currency exchange rates

primarily as a result of certain receivable and payable balances. The primary currency exchanges we have exposure to are the

Canadian dollar, the Chinese renminbi, the Mexican peso, the European euro, the British pound sterling and the Brazilian real. We

periodically enter into foreign exchange forward contracts to hedge some portion of our foreign currency exposure. A hypothetical

10% change in foreign exchange rates effective at October 3, 2009, and September 27, 2008, related to the foreign exchange forward

contracts would have a $15 million and $11 million, respectively, impact on pretax income. In the future, we may enter into more

foreign exchange forward contracts as a result of our international growth strategy.

Concentrations of Credit Risk: Our financial instruments exposed to concentrations of credit risk consist primarily of cash

equivalents and trade receivables. Our cash equivalents are in high quality securities placed with major banks and financial

institutions. Concentrations of credit risk with respect to receivables are limited due to our large number of customers and their

dispersion across geographic areas. We perform periodic credit evaluations of our customers’ financial condition and generally do not

require collateral. At October 3, 2009, and September 27, 2008, 13.0% and 12.2%, respectively, of our net accounts receivable

balance was due from Wal-Mart Stores, Inc. No other single customer or customer group represents greater than 10% of net accounts

receivable.