Time Magazine 2013 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2013 Time Magazine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

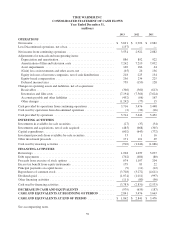

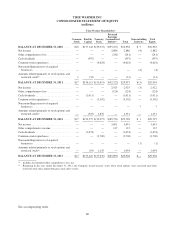

TIME WARNER INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

that the carrying value of Time Inc. will exceed its fair value, which could result in the Company recognizing a

noncash impairment of goodwill that could be material.

Long-Lived Assets

Long-lived assets, including finite-lived intangible assets (e.g., tradenames, customer lists, film libraries and

property, plant and equipment), do not require that an annual impairment test be performed; instead, long-lived

assets are tested for impairment upon the occurrence of a triggering event. Triggering events include the more

likely than not disposal of a portion of such assets or the occurrence of an adverse change in the market involving

the business employing the related assets. Once a triggering event has occurred, the impairment test is based on

whether the intent is to hold the asset for continued use or to hold the asset for sale. The impairment test for

assets held for continued use requires a comparison of cash flows expected to be generated over the useful life of

an asset or group of assets (“asset group”) against the carrying value of the asset group. An asset group is

established by identifying the lowest level of cash flows generated by the asset or group of assets that are largely

independent of the cash flows of other assets. If the intent is to hold the asset group for continued use, the

impairment test first requires a comparison of estimated undiscounted future cash flows generated by the asset

group against its carrying value. If the carrying value exceeds the estimated undiscounted future cash flows, an

impairment would be measured as the difference between the estimated fair value of the asset group and its

carrying value. Fair value is generally determined by discounting the future cash flows associated with that asset

group. If the intent is to hold the asset group for sale and certain other criteria are met (e.g., the asset can be

disposed of currently, appropriate levels of authority have approved the sale, and there is an active program to

locate a buyer), the impairment test involves comparing the asset group’s carrying value to its estimated fair

value. To the extent the carrying value is greater than the estimated fair value, an impairment loss is recognized

for the difference. Significant judgments in this area involve determining the appropriate asset group level at

which to test, determining whether a triggering event has occurred, determining the future cash flows for the

assets involved and selecting the appropriate discount rate to be applied in determining estimated fair value. For

more information, see Note 2.

Accounting for Pension Plans

Time Warner and certain of its subsidiaries have both funded and unfunded defined benefit pension plans,

the substantial majority of which are noncontributory, covering a majority of domestic employees and, to a lesser

extent, have various defined benefit plans, primarily noncontributory, covering certain international employees.

Pension benefits are based on formulas that reflect the participating employees’ years of service and

compensation. Time Warner uses a December 31 measurement date for its plans. The pension expense

recognized by the Company is determined using certain assumptions, including the expected long-term rate of

return on plan assets, the interest factor implied by the discount rate and the rate of compensation increases.

Additional information about the determination of pension-related assumptions is presented in Note 13.

Equity-Based Compensation

The Company measures the cost of employee services received in exchange for an award of equity

instruments based on the grant-date fair value of the award. That cost is recognized in Costs of revenues or

Selling, general and administrative expenses depending on the job function of the grantee on a straight-line basis

(net of estimated forfeitures) from the date of grant over the period during which an employee is required to

provide services in exchange for the award. The total grant-date fair value of an equity award granted to an

employee who has reached a specified age and years of service as of the grant date is recognized as compensation

expense immediately upon grant as there is no required service period.

The grant-date fair value of a restricted stock unit (“RSU”) is determined based on the closing sale price of

the Company’s common stock on the NYSE Composite Tape on the date of grant.

68