Time Magazine 2013 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2013 Time Magazine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

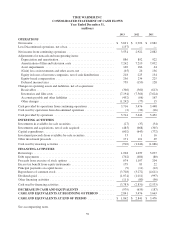

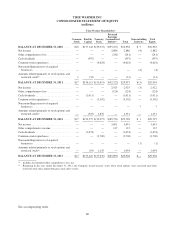

TIME WARNER INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

and, when applicable, various growth rates are assumed for years beyond the current long range plan period.

Discount rate assumptions are based on an assessment of market rates as well as the risk inherent in the future

cash flows included in the budgets and long range plans.

In 2013, the Company elected not to perform a qualitative assessment of Goodwill and instead proceeded to

perform a quantitative impairment test. The results of the quantitative test did not result in any impairments of

Goodwill because the fair values of each of the Company’s reporting units exceeded their respective carrying

values. The fair value of the Time Inc. reporting unit exceeded its carrying value by approximately 3%. No other

reporting unit’s fair value was within 10% of its carrying value. Had the fair value of the Time Inc. reporting unit

been hypothetically lower by 10% as of December 31, 2013, its carrying value would have exceeded its fair

value. Had the fair values of each of the Company’s reporting units been hypothetically lower by 20% as of

December 31, 2013, the Time Inc. and the Warner Bros. reporting units’ carrying values would have exceeded

their respective fair values. If this were to occur, the second step of the impairment review process would need to

be performed to determine the ultimate amount of impairment loss to record. For Time Inc., the significant

assumptions utilized in the 2013 DCF analysis were a discount rate of 10.5% and a terminal revenue growth rate

of 1.00%. Significant assumptions utilized for all other reporting units included discount rates that ranged from

9.5% to 10.0% and a terminal revenue growth rate of 3.25%. Significant assumptions utilized in the market-

based approach were market multiples of 7.5x for the Time Inc. reporting unit and market multiples ranging from

7.5x to 12.0x for the Company’s other reporting units where a market-based approach was performed.

In assessing other intangible assets not subject to amortization for impairment, the Company also has the

option to perform a qualitative assessment to determine whether the existence of events or circumstances leads to

a determination that it is more likely than not that the fair value of such an intangible asset is less than its

carrying amount. If the Company determines that it is not more likely than not that the fair value of such an

intangible asset is less than its carrying amount, then the Company is not required to perform any additional tests

for assessing those intangible assets for impairment. However, if the Company concludes otherwise or elects not

to perform the qualitative assessment, then it is required to perform a quantitative impairment test that involves a

comparison of the estimated fair value of the intangible asset with its carrying value. If the carrying value of the

intangible asset exceeds its fair value, an impairment loss is recognized in an amount equal to that excess.

In 2013, the Company elected not to perform a qualitative assessment for intangible assets not subject to

amortization. The estimates of fair value of intangible assets not subject to amortization are determined using a

DCF valuation analysis. Common among such approaches is the “relief from royalty” methodology, which is

used in estimating the fair value of the Company’s tradenames. Discount rate assumptions are based on an

assessment of the risk inherent in the projected future cash flows generated by the respective intangible assets.

Also subject to judgment are assumptions about royalty rates, which are based on the estimated rates at which

similar tradenames are being licensed in the marketplace.

The performance of the Company’s 2013 annual impairment test for other intangible assets not subject to

amortization resulted in the impairment of a tradename at Time Inc. As a result, the Company wrote down this

tradename from its carrying value of $539 million to its fair value of $489 million. No other tradename’s fair

value was within 20% of its carrying value. The significant assumptions utilized in the 2013 DCF analysis of

other intangible assets not subject to amortization at Time Inc. were a discount rate of 11.0% and a terminal

revenue growth rate of 1.00%, and for all other intangible assets not subject to amortization discount rates that

ranged from 10.0% to 10.5% and a terminal revenue growth rate of 3.25%.

Because of the planned spin-off of Time Inc., the Company will continue to perform interim impairment

reviews of Time Inc.’s goodwill during 2014 for the periods prior to the spin off. Time Inc. is experiencing

declines in its print advertising and newsstand sales as a result of market conditions in the publishing industry.

During the fourth quarter, senior management at Time Inc. prepared a new long-range plan that served as the

basis for the DCF analysis used in the 2013 annual impairment review. If market conditions worsen as compared

to the assumptions incorporated in that long-range plan, if market conditions associated with valuation multiples

of comparable companies decline, or if Time Inc.’s performance fails to meet current expectations, it is possible

67