Time Magazine 2013 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2013 Time Magazine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

TIME WARNER INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

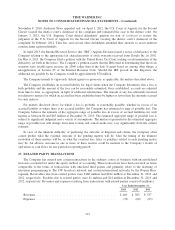

November 8, 2010, Anderson News appealed and, on April 3, 2012, the U.S. Court of Appeals for the Second

Circuit vacated the district court’s dismissal of the complaint and remanded the case to the district court. On

January 7, 2013, the U.S. Supreme Court denied defendants’ petition for writ of certiorari to review the

judgment of the U.S. Court of Appeals for the Second Circuit vacating the district court’s dismissal of the

complaint. In February 2014, Time Inc. and several other defendants amended their answers to assert antitrust

counterclaims against plaintiffs.

In April 2013, the Internal Revenue Service (the “IRS”) Appeals Division issued a notice of deficiency to the

Company relating to the appropriate tax characterization of stock warrants received from Google Inc. in 2002.

On May 6, 2013, the Company filed a petition with the United States Tax Court seeking a redetermination of the

deficiency set forth in the notice. The Company’s petition asserts that the IRS erred in determining that the stock

warrants were taxable upon exercise (in 2004) rather than at the date of grant based on, among other things, a

misapplication of Section 83 of the Internal Revenue Code. Should the IRS prevail in this litigation, the

additional tax payable by the Company would be approximately $70 million.

The Company intends to vigorously defend against or prosecute, as applicable, the matters described above.

The Company establishes an accrued liability for legal claims when the Company determines that a loss is

both probable and the amount of the loss can be reasonably estimated. Once established, accruals are adjusted

from time to time, as appropriate, in light of additional information. The amount of any loss ultimately incurred

in relation to matters for which an accrual has been established may be higher or lower than the amounts accrued

for such matters.

For matters disclosed above for which a loss is probable or reasonably possible, whether in excess of an

accrued liability or where there is no accrued liability, the Company has estimated a range of possible loss. The

Company believes the estimate of the aggregate range of possible loss in excess of accrued liabilities for such

matters is between $0 and $65 million at December 31, 2013. The estimated aggregate range of possible loss is

subject to significant judgment and a variety of assumptions. The matters represented in the estimated aggregate

range of possible loss will change from time to time and actual results may vary significantly from the current

estimate.

In view of the inherent difficulty of predicting the outcome of litigation and claims, the Company often

cannot predict what the eventual outcome of the pending matters will be, what the timing of the ultimate

resolution of these matters will be, or what the eventual loss, fines or penalties related to each pending matter

may be. An adverse outcome in one or more of these matters could be material to the Company’s results of

operations or cash flows for any particular reporting period.

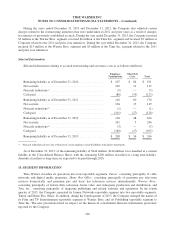

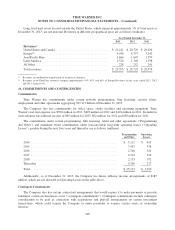

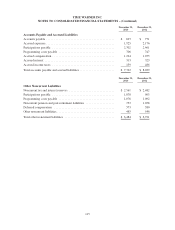

17. RELATED PARTY TRANSACTIONS

The Company has entered into certain transactions in the ordinary course of business with unconsolidated

investees accounted for under the equity method of accounting. These transactions have been executed on terms

comparable to the terms of transactions with unrelated third parties and primarily relate to the licensing of

television programming to The CW broadcast network and certain international networks by the Warner Bros.

segment. Receivables due from related parties were $186 million and $184 million at December 31, 2013 and

2012, respectively. Payables due to related parties were $1 million and $14 million at December 31, 2013 and

2012, respectively. Revenues and expenses resulting from transactions with related parties consist of (millions):

Year Ended December 31,

2013 2012 2011

Revenues .................................................... $ 469 $ 503 $ 537

Expenses .................................................... (35) (60) (63)

113