Pottery Barn 2012 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2012 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

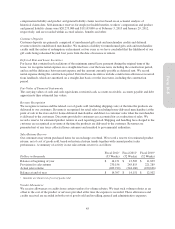

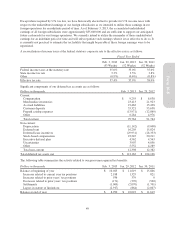

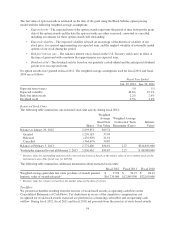

We review the carrying value of all long-lived assets for impairment, primarily at a store level, whenever events

or changes in circumstances indicate that the carrying value of an asset may not be recoverable. Our impairment

analyses determine whether projected cash flows from operations are sufficient to recover the carrying value of

these assets. Impairment may result when the carrying value of the asset exceeds the estimated undiscounted

future cash flows over its remaining useful life. For store impairment, our estimate of undiscounted future cash

flows over the store lease term is based upon our experience, historical operations of the stores and estimates of

future store profitability and economic conditions. The future estimates of store profitability and economic

conditions require estimating such factors as sales growth, gross margin, employment rates, lease escalations,

inflation and the overall economics of the retail industry, and are therefore subject to variability and difficult to

predict. Actual future results may differ from those estimates. If a long-lived asset is found to be impaired, the

amount recognized for impairment is equal to the difference between the asset’s net carrying value and its fair

value. Long-lived assets are measured at fair value on a nonrecurring basis using Level 3 inputs as defined in the

fair value hierarchy. The fair value is estimated based upon the present value of estimated future cash flows

(discounted at a rate commensurate with the risk and that approximates our weighted average cost of capital).

For any store or facility closure where a lease obligation still exists, we record the estimated future liability

associated with the rental obligation on the cease use date.

During fiscal 2012, we recorded expense of approximately $6,071,000 associated with asset impairment charges,

primarily related to underperforming retail stores, all of which is recorded within selling, general and

administrative expenses.

During fiscal 2011, we recorded expense of approximately $3,194,000 associated with asset impairment and

early lease termination charges for underperforming retail stores, substantially all of which is recorded within

selling, general and administrative expenses.

During fiscal 2010, we recorded expense of approximately $17,525,000 associated with asset impairment and

early lease termination charges for underperforming retail stores, substantially all of which is recorded within

selling, general and administrative expenses. We also recorded a net benefit of $403,000 associated with the exit

of excess distribution capacity, which is recorded within selling, general and administrative expenses.

Goodwill

Goodwill is not amortized, but rather is subject to impairment testing annually (on the first day of the fourth

quarter), or between annual tests whenever events or changes in circumstances indicate that the fair value of a

reporting unit may be below its carrying amount. The first step of the impairment test requires determining the

fair value of the reporting unit. We use the income approach, whereby we estimate the fair value based on the

present value of estimated future cash flows. The process of evaluating the potential impairment of goodwill is

subjective and requires significant estimates and assumptions such as estimates for sales growth, gross margins,

employment rates, inflation and future economic and market conditions. Actual future results may differ from

those estimates. If the carrying value of the reporting unit’s assets and liabilities, including goodwill, is in excess

of its fair value, goodwill may be impaired, and we must perform a second step of comparing the implied fair

value of the goodwill to its carrying value to determine the impairment charge, if any. At February 3, 2013 and

January 29, 2012, we had goodwill of $18,951,000 and $19,301,000, respectively, included in other assets,

primarily related to our fiscal 2011 acquisition of Rejuvenation. We did not recognize any goodwill impairment

in fiscal 2012 or fiscal 2011.

Self-Insured Liabilities

We are primarily self-insured for workers’ compensation, employee health benefits and product and general

liability claims. We record self-insurance liabilities based on claims filed, including the development of those

claims, and an estimate of claims incurred but not yet reported. Factors affecting this estimate include future

inflation rates, changes in severity, benefit level changes, medical costs and claim settlement patterns. Should a

different amount of claims occur compared to what was estimated, or costs of the claims increase or decrease

beyond what was anticipated, reserves may need to be adjusted accordingly. We determine our workers’

44