Pottery Barn 2012 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2012 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

bonuses would be available if this goal was met, the Compensation Committee uses its discretion to determine

the actual amount, if any, to be paid to any named executive officer. See below for a discussion of whether and

how the Compensation Committee utilizes its discretion to determine actual bonus amounts.

Why did the Compensation Committee choose positive net cash flow provided by operating activities as the

primary performance goal under the Bonus Plan?

The Compensation Committee chose positive net cash flow provided by operating activities as the primary

performance goal for fiscal 2012 because it believed that maintaining positive net cash flow was critical to the

success of the company in fiscal 2012. The achievability of the goal was deemed substantially uncertain for

purposes of Internal Revenue Code Section 162(m). When the positive net cash flow objective for fiscal 2012

was first established, it was thought to be reasonably attainable, but not certain, based upon the company’s net

cash flow history and expected levels of net cash flow.

Did the company achieve positive net cash flow provided by operating activities for fiscal 2012?

Yes. For fiscal 2012, the company achieved positive net cash flow provided by operating activities as described

above. Since this primary, critical performance goal was achieved, maximum bonuses became available under

the Bonus Plan for fiscal 2012 for each named executive officer. As described below, the Compensation

Committee used discretion to decrease bonuses actually awarded under the Bonus Plan to significantly below the

maximum available levels for all named executive officers, other than Ms. McCollam and Mr. Harvey, who did

not receive bonuses. Please see below for a summary of the severance Ms. McCollam received.

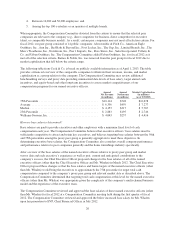

How does the Compensation Committee decide if and how to make bonus awards less than the maximum allowed

under the Bonus Plan?

The primary performance goal results in the funding of the Bonus Plan. If the primary performance goal is

achieved, as it was in fiscal 2012, then the Compensation Committee decides whether (and how) to reduce

bonuses from the maximum available under the Bonus Plan. In determining actual bonus awards, the

Compensation Committee evaluates company performance against a secondary performance goal. For fiscal

2012, this secondary goal was an earnings per share target of $2.52, with maximum funding at earnings per share

of $2.80 (excluding extraordinary non-recurring charges). Actual performance for fiscal 2012 exceeded this

secondary goal. Additionally, the Committee evaluates performance against the Company’s business plan that

was approved by the Board prior to the first fiscal quarter, and individual performance as assessed by the Chief

Executive Officer (for positions other than her own). The Compensation Committee may deviate from the

guidelines, but bonuses granted under the Bonus Plan may not exceed the maximum limit set forth in the plan.

Individual performance also is taken into account in determining appropriate bonus awards. Individual

performance is assessed by the Chief Executive Officer (for positions other than her own) and takes into account

achievement of individual goals and objectives. Achievement of objectives that increase stockholder return or

that are determined by the Chief Executive Officer (for positions other than her own) to significantly impact

future stockholder return are significant factors in the Chief Executive Officer’s individual performance

assessment. The Chief Executive Officer recommended bonus awards based on her assessment of the results

achieved by each named executive officer.

The Compensation Committee believes that achieving individual goals and objectives is important to the overall

success of the company and will adjust bonuses paid to reflect performance in these areas. For example, if the

company or an executive officer fails to fully meet some or all of the company or individual objectives, the

executive’s award may be significantly reduced or even eliminated. Conversely, if the objectives are

overachieved, awards may be subject to less or no reduction from the maximum available awards.

28