PG&E 2008 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2008 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

120

DIVIDEND PARTICIPATION RIGHTS

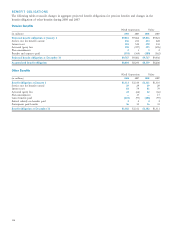

The dividend participation rights of the Convertible

Subordinated Notes are embedded derivative instruments in

accordance with SFAS No. 133 and, therefore, are bifurcated

from Convertible Subordinated Notes and recorded at fair

value in PG&E Corporation’s Consolidated Balance Sheets.

The dividend participation rights are valued based on the

net present value of estimated future cash fl ows using internal

estimates of future common stock dividends. The fair value

of the dividend participation rights is recorded as Current

Liabilities-Other and Noncurrent Liabilities-Other in PG&E

Corporation’s Consolidated Balance Sheets. (See Note 4

of the Notes to the Consolidated Financial Statements for

further discussion of these instruments.)

FINANCIAL INSTRUMENTS

PG&E Corporation and the Utility use the following

methods and assumptions in estimating fair value for

fi nancial instruments:

• The fair values of cash and cash equivalents, restricted cash

and deposits, net accounts receivable, price risk manage-

ment assets and liabilities, short-term borrowings, accounts

payable, customer deposits, and the Utility’s variable rate

pollution control bond loan agreements approximate their

carrying values as of December 31, 2008 and 2007.

• The fair values of the Utility’s fi xed rate senior notes, fi xed

rate pollution control bond loan agreements, and the ERBs

issued by PG&E Energy Recovery Funding LLC, were based

on quoted market prices obtained from the Bloomberg

fi nancial information system at December 31, 2008.

• The estimated fair value of PG&E Corporation’s 9.50%

Convertible Subordinated Notes was determined by con-

sidering the prices of securities displayed as of the close

of business on December 31, 2008 by a proprietary bond

trading system that tracks and marks a broad universe of

convertible securities including the securities being assessed.

CRRs allow market participants, including load serving

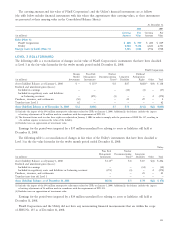

entities, to hedge fi nancial risk of CAISO-imposed congestion

charges in the day-ahead market to be established when MRTU

becomes effective. Firm Transmission Rights (“FTRs”) allow

market participants, including load serving entities, to hedge

both the physical and fi nancial risk associated with CAISO-

imposed congestion charges until the MRTU becomes effec-

tive. The Utility’s demand response contracts (“DRs”) with

third-party aggregators of retail electricity customers contain

a call option entitling the Utility to require that the aggre-

gator reduce electric usage by the aggregator’s customers at

times of peak energy demand or in response to a CAISO

alert or other emergency. As the market for CRRs, FTRs,

and DRs has minimal activity, observable inputs may

not be available in pricing these instruments. Therefore,

the pricing models used to value these instruments often

incorporate signifi cant estimates and assumptions that

market participants would use in pricing the instrument.

Accordingly, they are classifi ed as Level 3 measurements.

When available, observable market data is used to calibrate

pricing models.

Exchange-traded derivative instruments (other than

options) are generally valued based on unadjusted prices

in active markets using pricing models to determine the

net present value of estimated future cash fl ows. Accordingly,

a majority of these instruments are classifi ed as Level 1

measurements. However, certain of these exchange-traded

contracts are classifi ed as Level 2 measurements because the

contract term extends to a point at which the market is no

longer considered active but where prices are still observable.

This determination is based on an analysis of the relevant

characteristics of the market such as trading hours, trading

volumes, frequency of available quotes, and open interest.

In addition, a number of OTC contracts have been valued

using unadjusted exchange prices in active markets. Such

instruments are classifi ed as Level 2 measurements as they

are not exchange-traded instruments. The remaining OTC

derivative instruments are valued using pricing models based

on the net present value of estimated future cash fl ows

based on broker quotations. Such instruments are generally

classifi ed within Level 3 of the fair value hierarchy as broker

quotes are only indicative of market activity and do not

necessarily refl ect binding offers to transact.

See Note 11 of the Notes to the Consolidated Financial

Statements for further discussion of the price risk manage-

ment instruments.