OfficeMax 2009 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2009 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

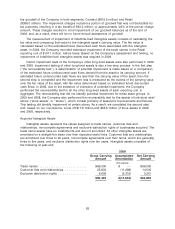

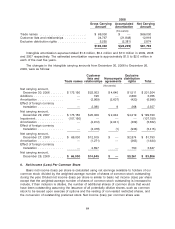

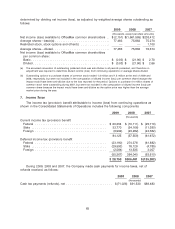

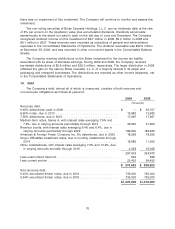

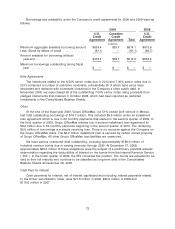

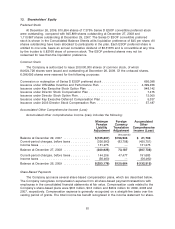

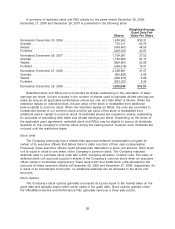

11. Financial Instruments, Derivatives and Hedging Activities

Fair Value of Financial Instruments

The carrying amounts of cash and cash equivalents, trade accounts receivable, other assets

(non-derivatives), short-term borrowings, trade accounts payable, and due to related party,

approximate fair value because of the short maturity of these instruments. The following table

presents the carrying amounts and estimated fair values of the Company’s other financial

instruments at December 26, 2009 and December 27, 2008. The fair value of a financial instrument

is the amount at which the instrument could be exchanged in a current transaction between willing

parties.

2009 2008

Carrying amount Fair value Carrying amount Fair value

(thousands)

Financial assets:

Timber notes receivable

Wachovia— ........... $817.5 $823.6 $817.5 $801.9

Lehman— ............ 81.8 81.8 81.8 81.8

Financial liabilities:

Debt .................... $297.6 $207.2 $355.0 $236.7

Timber securitization notes

Wachovia— ........... $735.0 $754.8 $735.0 $736.8

Lehman— ............ 735.0 81.8 735.0 81.8

In establishing a fair value, there is a fair value hierarchy that prioritizes the inputs to valuation

techniques used to measure fair value. The basis of the fair value measurement is categorized in

three levels, in order of priority, described as follows:

Level 1: Unadjusted quoted prices in active markets that are accessible at the measurement

date for identical, unrestricted assets or liabilities.

Level 2: Quoted prices in markets that are not active, or financial instruments for which all

significant inputs are observable; either directly or indirectly.

Level 3: Prices or valuation techniques that require inputs that are both significant to the fair

value measurement and unobservable; thus reflecting assumptions about the market participants.

The carrying amounts shown in the table are included in the Consolidated Balance Sheets

under the indicated captions. The following methods and assumptions were used to estimate the

fair value of each class of financial instruments:

• Timber notes receivable: The fair value of the Wachovia Guaranteed Installment Notes is

determined as the present value of expected future cash flows discounted at the current

interest rate for loans of similar terms with comparable credit risk (Level 2 inputs). The fair

value of the Lehman Guaranteed Installment Note reflects the estimated future cash flows of

the note considering the estimated effects of the Lehman bankruptcy (Level 3 inputs).

• Debt: The fair value of the Company’s debt is estimated based on quoted market prices

when available or by discounting the future cash flows of each instrument at rates currently

offered to the Company for similar debt instruments of comparable maturities (Level 2

inputs).

• Timber securitization notes: The fair value of the Securitization Notes supported by Wachovia

is estimated by discounting the future cash flows of the instrument at rates currently available

73