OfficeMax 2009 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2009 OfficeMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

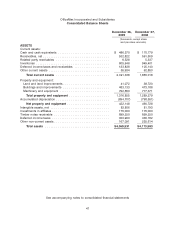

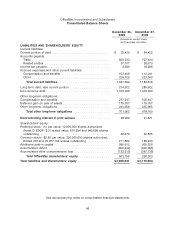

Goodwill, Indefinite-Lived Intangibles and Other Long-Lived Assets Impairment

Generally accepted accounting principles (‘‘GAAP’’) require us to assess intangible assets for

impairment at least annually in the absence of an indicator of possible impairment and immediately

upon an indicator of possible impairment. In assessing impairment, we are required to make

estimates of the fair values the assets. If we determine the fair values are less than the carrying

amount recorded on our Consolidated Balance Sheet, we must recognize an impairment loss in our

financial statements. We are also required to assess our long-lived assets for impairment whenever

an indicator of possible impairment exists. In assessing impairment, the statement requires us to

make estimates of the fair value of the assets. If we determine the fair values are less than the

carrying value of the assets, we must recognize an impairment loss in our financial statements.

The measurement of impairment of indefinite life intangibles and other long-lived assets

includes estimates and assumptions which are inherently subject to significant uncertainties. In

testing for impairment, we measure the estimated fair value of our reporting units, intangibles and

fixed assets based upon discounted future operating cash flows using a discount rate reflecting a

market-based, weighted average cost of capital. In estimating future cash flows, we use our internal

budgets and operating plans, which include many assumptions about future growth prospects,

margin rates, and cost factors. Differences in assumptions used in projecting future operating cash

flows and in selecting an appropriate discount rate could have a significant impact on the

determination of fair value and impairment amounts.

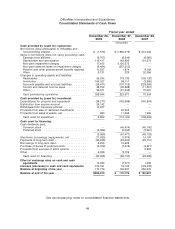

Recently Issued or Newly Adopted Accounting Standards

Following are summaries of recently issued accounting pronouncements that have either been

recently adopted or that may become applicable to the preparation of our consolidated financial

statements in the future.

In June 2009, the Financial Accounting Standards Board (‘‘FASB’’) issued a statement

establishing the FASB Accounting Standards Codification (‘‘the ASC’’ or ‘‘the Codification’’).

Effective for interim and annual periods ended after September 15, 2009, the Codification became

the source of authoritative U.S. GAAP recognized by the FASB to be applied by nongovernmental

entities. Rules and interpretive releases of the SEC under authority of federal securities laws are

also sources of authoritative GAAP for SEC registrants. This statement is not intended to change

existing GAAP and as such did not have an impact on the consolidated financial statements of the

Company. The Company has updated its references to reflect the Codification.

In September 2006, the FASB issued guidance which defines fair value, establishes a

framework for measuring fair value in generally accepted accounting principles and expands

disclosures about fair value measurements. This guidance was effective for fiscal years beginning

after November 15, 2007, for financial assets and liabilities, as well as for any other assets and

liabilities that are carried at fair value on a recurring basis in the financial statements. In November

2007, the FASB provided a one year deferral for the implementation of this guidance for other

nonfinancial assets and liabilities. The Company adopted this guidance for financial assets and

liabilities effective at the beginning of fiscal year 2008 and for non-financial assets and liabilities

effective at the beginning of fiscal year 2009. The adoption of this guidance had no significant

impact on our consolidated financial statements for either fiscal year 2008 or 2009.

In December 2007, the FASB issued updated guidance which changed the presentation and

disclosure requirements for noncontrolling interests (previously referred to as minority interests).

This updated guidance is effective for periods beginning on or after December 15, 2008, and is to

be applied prospectively to all noncontrolling interests, including those that arose prior to the

effective date. While the accounting requirements are to be applied prospectively, prior period

financial information must be recast to attribute net income and other comprehensive income to

44