NetSpend 2013 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2013 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84

|

|

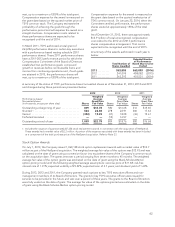

combining the operations of TSYS and CPAY. All of

the goodwill is tax deductible.

The following table summarizes the consideration

paid for acquisitions and the preliminary recognized

amounts of identifiable assets acquired and liabilities

assumed during the year ended December 31, 2012.

(in thousands)

Cash and restricted cash .............. $ 3,003

Accounts receivable .................. 4,092

Other assets ........................ 12,522

Identifiable intangible assets ........... 76,600

Other liabilities ...................... (30,558)

Noncontrolling interest in acquired

entity ............................ (38,000)

Goodwill ........................... 162,090

Total consideration ................. $189,749

The fair value of accounts receivable, accounts

payable, accrued compensation, and other liabilities

approximates the carrying amount of those assets

and liabilities at the acquisition date. The fair value of

accounts receivable due under agreements with

customers is $4.1 million. The gross amount due

under the agreements is $4.8 million, of which

approximately $688,000 is expected to be

uncollectible.

Of the $123.7 million in consideration paid for

ProPay, $12.5 million has been placed in escrow for a

period of 18 months to secure certain claims that may

be brought against the escrowed consideration by

TSYS pursuant to the merger agreement.

Consideration is contingent and may be returned to

the Company pursuant to indemnification

commitments made by the shareholders which

formerly owned ProPay related to a breach of the

representations and warranties made in the merger

agreement. Such indemnification commitments are

recognized as a possible receivable and measured at

fair value. Based upon the probability of various

possible outcomes related to the indemnification

commitments, TSYS has determined that the fair

value of any receivable asset would be immaterial.

The maximum amount of contingent consideration

returnable to the Company related to certain

indemnification commitments made by the Seller is

$12.5 million. The maximum amount of contingent

consideration returnable to the Company related to

fundamental representations and warranties made by

the Seller is unlimited.

Of the $66 million in consideration paid for CPAY,

$3.3 million has been placed in escrow for a period of

21 months to secure certain claims that may be

brought against the escrowed consideration by TSYS

pursuant to the Investment Agreement.

Consideration is contingent and may be returned to

the Company pursuant to indemnification

commitments made by the company which formerly

owned 100% of Central Payment (Seller) related to,

among other things, a breach of the representations

and warranties made in the Investment Agreement,

and losses arising out of any of the Excluded

Liabilities as defined in the Investment Agreement.

Such indemnification commitments are recognized as

a possible asset receivable and measured at fair

value. Based upon the probability of various possible

outcomes related to the indemnification

commitments, TSYS has determined that the fair

value of any receivable asset would be immaterial.

The maximum amount of contingent consideration

returnable to the Company related to certain

indemnification commitments made by the Seller is

$9.9 million. The maximum amount of contingent

consideration returnable to the Company related to

fundamental representations and warranties made by

the Seller is unlimited.

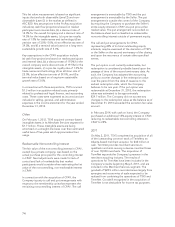

Identifiable intangible assets acquired in the

acquisitions had no significant estimated residual

value. These intangible assets are being amortized

over their estimated useful lives of 2 to 10 years

based on the pattern of expected future economic

benefit, which approximates a straight-line basis over

the useful lives of the assets. The fair value of the

acquired identifiable intangible assets of $76.6

million was estimated using the income approach

(discounted cash flow and relief from royalty

methods) and cost approach. The fair values and

useful lives of the identified intangible assets were

primarily determined using forecasted cash flows,

which included estimates for certain assumptions

such as revenues, expenses, attrition rates, and

royalty rates. The estimated fair value of identifiable

intangible assets acquired in the acquisitions and the

related estimated weighted average useful lives are

as follows:

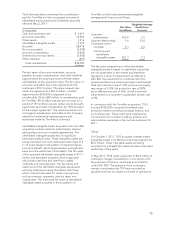

Fair Value

(in millions)

Weighted Average

Useful Lives

(in years)

Customer

relationships ......... $59.5 8.6

Covenants-not-to-

compete ............ 2.9 2.8

Current technology ..... 13.0 5

Trade name ........... 1.2 2

Total acquired

identifiable

intangible assets . . . $76.6 7.7

73