NetSpend 2013 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2013 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

On May 22, 2013, the Company closed its issuance

(the “Transaction”) of $550.0 million aggregate

principal amount of 2.375% Senior Notes due 2018

and $550.0 million aggregate principal amount of

3.750% Senior Notes due 2023 (collectively, the

“Notes”) pursuant to an Underwriting Agreement

with J.P. Morgan Securities LLC, as representative of

certain underwriters (the “Underwriters”), whereby

the Company agreed to sell and the Underwriters

agreed to purchase the Notes from the Company,

subject to and upon the terms and conditions set

forth in the Underwriting Agreement. The interest on

the Notes are payable semiannually. The Company

paid fees associated with the issuance of these Notes

of approximately $8.9 million and recorded discounts

of approximately $4.3 million that are being

amortized over the life of the Notes. The Company

used the net proceeds of the Transaction to pay a

portion of the $1.4 billion purchase price of the

Company’s acquisition of NetSpend and related fees

and expenses. The Notes were issued pursuant to an

Indenture dated as of May 22, 2013 between the

Company and Wells Fargo Bank, National

Association, as trustee. The Company received a

rating from Moody’s of Baa3 and a rating from

Standard & Poor’s of BBB+ in connection with the

Senior Notes at the time of issuance.

The Notes also contain various affirmative and

negative covenants, including those that create

limitations on the Company’s:

• creation of liens;

• merging or selling assets unless certain

conditions are met; and

• entering into sale/leaseback transactions.

The Notes also contain a provision that requires the

Company to repurchase all or any portion of a

holder’s Notes, at the holder’s option, if a Change in

Control Repurchase Event occurs.

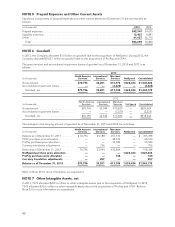

Amendment to Existing Credit Agreement

On September 10, 2012, the Company entered into a

credit agreement with JPMorgan Chase Bank, N.A.,

as Administrative Agent, The Bank of Tokyo-

Mitsubishi UFJ, Ltd., Regions Bank and U.S. Bank

National Association, as Syndication Agents, and the

other lenders named therein, with J.P. Morgan

Securities LLC, The Bank of Tokyo-Mitsubishi UFJ,

Ltd., Regions Capital Markets and U.S. Bank National

Association, as joint lead arrangers and joint

bookrunners (the “Existing Credit Agreement”). The

Existing Credit Agreement provides for a

$350 million five-year unsecured revolving credit

facility (which may be increased by up to an

additional $350 million under certain circumstances)

and includes a $50 million subfacility for the issuance

of standby letters of credit and a $50 million

subfacility for swingline loans. The Existing Credit

Agreement also provides for a $150 million five-year

unsecured term loan, which was fully funded on the

closing of the Existing Credit Agreement. As of

December 31, 2013, the outstanding balance on the

Existing Credit Agreement was $138.8 million.

On April 8, 2013, the Company entered into the First

Amendment to the Existing Credit Agreement (the

“Revolver”) in order to conform certain provisions of

the Existing Credit Agreement to the Credit

Agreement for the Term Loan. On July 1, 2013, an

additional $100 million was used as funding in the

NetSpend Merger. As of December 31, 2013, there

was no outstanding balance on the Revolver.

On September 10, 2012 and in connection with

entering into the credit facilities described above, the

Company terminated its existing credit agreement

dated as of December 21, 2007 with Bank of America

N.A., as Administrative Agent, The Royal Bank of

Scotland plc, as Syndication Agent, and the other

lenders named therein. That credit agreement

provided for a $252 million five-year unsecured

revolving credit facility and a $168 million five-year

term loan, both of which were scheduled to mature

on December 21, 2012. No material early termination

penalties were incurred as a result of the termination.

The Credit Agreement for the aforementioned loan

provided for a $168 million unsecured five year term

loan to the Company and a $252 million five year

unsecured revolving credit facility. The principal

balance of loans outstanding under the credit facility

bears interest at a rate of LIBOR plus an applicable

margin of 0.60%. The applicable margin could vary

within a range from 0.27% to 0.725% depending on

changes in the Company’s corporate credit rating.

Interest was paid on the last date of each interest

period; however, if the period exceeded three

months, interest was paid every three months after

the beginning of such interest period. In addition, the

Company paid each lender a fee in respect of the

amount of such lender’s commitment under the

revolving credit facility (regardless of usage), ranging

from 0.08% to 0.15% (currently 0.10%) depending on

the Company’s corporate credit rating.

The Company was not required to make any

scheduled principal payments other than payment of

the entire outstanding balance on December 21,

2012. The Company was able to prepay the revolving

52