NetSpend 2013 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2013 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

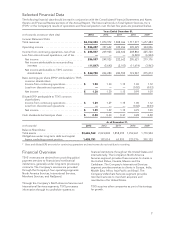

TSYS’ revenues are generated primarily from charges

based on the number of accounts on file (AOF),

transactions and authorizations processed,

statements mailed, cards embossed and mailed, and

other processing services for cardholder AOF.

Cardholder AOF include active and inactive

consumer credit, retail, prepaid, stored value,

government services and commercial card accounts.

TSYS’ revenues in its North America Services and

International Services segments are influenced by

several factors, including volumes related to AOF and

transactions. TSYS estimates that approximately

49.6% of these segments’ revenues is AOF and

transaction volume driven. The remaining 50.4% of

payment processing revenues are not AOF and

transaction volume driven, and are derived from

production and optional services TSYS considers to

be value added products and services, custom

programming and licensing arrangements.

Whether or not an account on file is active can impact

TSYS’ revenues differently. Active accounts are

accounts that have had monetary activity either

during the current month or in the past 90 days

based on contractual definition. Inactive accounts are

accounts that have not had a monetary transaction

(such as a purchase or payment) in the past 90 days.

The more active an account is, the more revenue is

generated for TSYS (items such as transactions and

authorizations processed and statements billed).

Occasionally, a client will purge inactive accounts

from its portfolio. An inactive account typically will

only generate an AOF charge. A processing client will

periodically review its cardholder portfolio based

upon activity and usage. Each client, based upon

criteria individually set by the client, will flag an

account to be “purged” from TSYS’ system and

deactivated.

A deconversion involves a client migrating all of its

accounts to an in-house solution or another

processor. Account deconversions include active and

inactive accounts and can impact the Company’s

revenues significantly more than an account purge.

A sale of a portfolio typically involves a client selling a

portion of its accounts to another party. A sale of a

portfolio and a deconversion impact the Company’s

financial statements in a similar fashion, although a

sale usually has a smaller financial impact due to the

number of accounts typically involved.

TSYS’ revenues in its Merchant Services segment are

influenced by several factors, including volumes

related to transactions and dollar sales volume, which

are approximately 93.4% of this segment’s revenues.

The remaining 6.6% of Merchant Services’ revenues

are derived from value added services, monthly

statement fees, compliance fees, and miscellaneous

services.

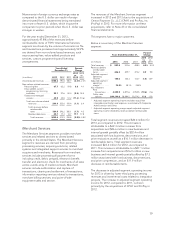

TSYS’ revenues in its NetSpend segment primarily

consist of a portion of the service fees and

interchange revenues received by NetSpend’s

prepaid card Issuing Banks in connection with the

programs managed by NetSpend. For the year

ended December 31, 2013, 74.9% of revenues was

derived from fees charged to cardholders and 25.1%

of revenues was derived from interchange. Service

fee revenues are driven by the number of active

cards, and in particular by the number of cards with

direct deposit. Cardholders with direct deposit

generally initiate more transactions and generate

more revenues than those that do not take

advantage of this feature. Interchange revenues are

driven by gross dollar volume. Substantially all of the

NetSpend segment’s revenues are volume driven as

they are driven by the active card and gross dollar

volume indicators.

14