IHOP 2014 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2014 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

DineEquity, Inc. and Subsidiaries

Notes to the Consolidated Financial Statements (Continued)

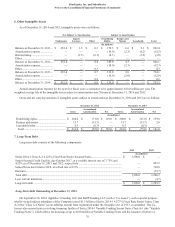

7. Long-Term Debt (Continued)

80

In addition, Amendment No. 2 established the following consolidated leverage ratio thresholds for excess cash flow

prepayments: 50% if the consolidated leverage ratio is 5.75:1 or greater; 25% if the consolidated leverage ratio is less than

5.75:1 and greater than or equal to 5.25:1; and 0% if the consolidated leverage ratio is less than 5.25:1.

Amendment No. 2 revised the definition of excess cash flow to eliminate the deduction for any extraordinary receipts or

disposition proceeds. Finally, Amendment No. 2 revised the definition of certain permitted payments so that the calculation of

allowable restricted payments is performed on a quarterly basis instead of an annual basis that was required prior to

Amendment No. 2. All other material provisions, including maturity and covenants under the Credit Agreement, remain

unchanged.

Fees of $1.3 million paid to third parties in connection with Amendment No. 2 were included as “Debt modification costs”

in the Consolidated Statement of Comprehensive Income for the year ended December 31, 2013.

Guarantees

The loans made under the Credit Agreement were guaranteed by the Company's domestic wholly-owned restricted

subsidiaries, other than immaterial subsidiaries (the “Prior Guarantors”), and were secured by a perfected first priority security

interest in substantially all of the tangible and intangible assets of the Company and the Prior Guarantors, including, without

limitation, (i) substantially all personal, real and mixed property, (ii) all intercompany debt owing to the Company and the Prior

Guarantors and (iii) 100% of the equity interests held by the Company and each of the Prior Guarantors (with customary limits

for foreign subsidiaries), subject to certain customary exceptions.

Mandatory Prepayments

Term Loans under the Credit Agreement were subject to the following prepayment requirements:

• Mandatory prepayments equal to 0.25% of the aggregate principal amount of the New Term Loan had to be made on a

quarterly basis (1.0% for a fiscal year); and

• 50% of excess cash flow (as defined in the Credit Agreement or amendments thereto) if the consolidated leverage ratio is

5.75:1 or greater; 25% if the consolidated leverage ratio is less than 5.75:1 and greater than or equal to 5.25:1; and 0% if

the consolidated leverage ratio is less than 5.25:1.

The Credit Agreement permitted the Company to purchase loans under the Term Facility pursuant to customary Dutch

auction provisions and subject to customary conditions and limitations.

Covenants/Restrictions

The Credit Agreement required the Company to comply with certain financial covenants, including a minimum

consolidated interest coverage ratio and a maximum consolidated leverage ratio, in each case, commencing with the fiscal

quarter ending March 31, 2011. The Credit Agreement also included certain negative covenants customary for transactions of

this type, that restricted the ability of the Company and the Company's existing and future restricted subsidiaries to, among

other things, modify material agreements and/or incur additional debt, incur liens, make certain investments and acquisitions,

make fundamental changes, transfer and sell assets, pay dividends and make distributions, modify the nature of the Company's

business, enter into agreements with shareholders and affiliates, enter into burdensome agreements, change the Company's

fiscal year, make capital expenditures and prepay certain indebtedness, subject to certain customary exceptions, including

carve-outs and baskets.

The Credit Agreement contained certain customary representations and warranties, affirmative covenants and events of

default, including change of control provisions and cross-defaults to other debt. Upon the occurrence of an event of default, the

lenders, by a majority vote, had the ability to direct the Administrative Agent to terminate the loan commitments, accelerate all

loans and exercise any of the lenders' other rights under the Credit Agreement and the related loan documents on behalf of the

lenders.

9.5% Senior Notes due 2018

On October 19, 2010, the Company issued $825.0 million aggregate principal amount of its 9.5% Senior Notes due

October 30, 2018 (the “Senior Notes”) pursuant to an Indenture (the “Senior Note Indenture”), by and among the Company, the

Guarantors and Wells Fargo Bank, National Association, as trustee (the “Trustee”). The Senior Notes were unsecured senior