IHOP 2014 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2014 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

DineEquity, Inc. and Subsidiaries

Notes to the Consolidated Financial Statements (Continued)

7. Long-Term Debt (Continued)

78

Guarantees and Collateral

Under the Guarantee and Collateral Agreement dated September 30, 2014 (the “Guarantee and Collateral Agreement”),

among the Guarantors in favor of the Trustee, the Guarantors guarantee the obligations of the Co-Issuers under the Indenture

and related documents and secure the guarantee by granting a security interest in substantially all of their assets.

The Notes are secured by a security interest in substantially all of the assets of the Co-Issuers and the Guarantors

(collectively, the “Securitization Entities”). On September 30, 2014, these assets (the “Securitized Assets”) generally included

substantially all of the domestic revenue-generating assets of the Corporation and its subsidiaries, which principally consist of

franchise agreements, area license agreements, development agreements, franchisee fee notes, equipment leases, agreements

related to the production and sale of pancake and waffle dry-mixes, owned and leased real property and intellectual property.

The Notes are obligations only of the Co-Issuers pursuant to the Indenture and are unconditionally and irrevocably

guaranteed by the Guarantors pursuant to the Guarantee and Collateral Agreement. Except as described below, neither we nor

any of our subsidiaries, other than the Securitization Entities, will guarantee or in any way be liable for the obligations of the

Co-Issuers under the Indenture or the Notes.

Covenants and Restrictions

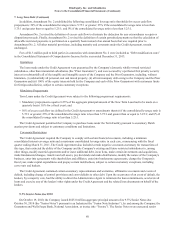

The Notes are subject to a series of covenants and restrictions customary for transactions of this type, including (i) that the

Co-Issuers maintain specified reserve accounts to be used to make required payments in respect of the Notes, (ii) provisions

relating to optional and mandatory prepayments, and the related payment of specified amounts, including specified make-whole

payments in the case of the Class A-2 Notes under certain circumstances, (iii) certain indemnification payments in the event,

among other things, the transfers of the assets pledged as collateral for the Notes are in stated ways defective or ineffective and

(iv) covenants relating to recordkeeping, access to information and similar matters. The Notes are also subject to customary

rapid amortization events provided for in the Indenture, including events tied to failure of the Securitization Entities to maintain

the stated debt service coverage (“DSCR”) ratio, the sum of domestic retail sales for all restaurants being below certain levels

on certain measurement dates, certain manager termination events, certain events of default and the failure to repay or refinance

the Notes on the Class A-2 Anticipated Repayment Date. The Notes are also subject to certain customary events of default,

including events relating to non-payment of required interest, principal or other amounts due on or with respect to the Notes,

failure of the Securitization Entities to maintain the stated debt service coverage ratio, failure to comply with covenants within

certain time frames, certain bankruptcy events, breaches of specified representations and warranties and certain judgments.

The DSCR ratio is Net Cash Flow for the four quarters preceding the calculation date divided by the total debt service

payments of the preceding four quarters. Failure to maintain a prescribed DSCR ratio can trigger a Cash Trapping Event, A

Rapid Amortization Event, a Manager Termination Event or a Default Event as described below. In a Cash Trapping Event, the

Trustee is required to retain a certain percentage of cash flow in a restricted account. In a Rapid Amortization Event, all excess

Cash Flow is retained and used to retire principal amounts of debt. Key DSCR ratios are as follows:

• DSCR less than 1.75x but equal to or greater than 1.50x - Cash Trapping Event, 50% of Net Cash Flow

• DSCR less than 1.50x - Cash Trapping Event, 100% of Net Cash Flow

• DSCR less than 1.30x - Rapid Amortization Event

• DSCR less than 1.20x - Manager Termination Event

• DSCR less than 1.10x - Default Event

The DSCR for the reporting period ended December 31, 2014 was 4.9x.

Deferred Financing Costs

The Company incurred costs of approximately $24.3 million in connection with the issuance of the Notes. These deferred

financing costs will be amortized using the effective interest method over estimated life of the Notes. Amortization of these

deferred financing costs of $0.8 million was included in interest expense for the year ended December 31, 2014. Unamortized

deferred financing costs of $23.5 million was included as other non-current assets, net in the consolidated balance sheet as of

December 31, 2014.