IHOP 2014 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2014 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

DineEquity, Inc. and Subsidiaries

Notes to the Consolidated Financial Statements (Continued)

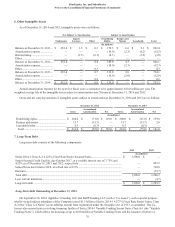

7. Long-Term Debt (Continued)

82

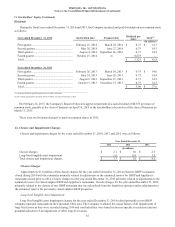

Deferred Financing Costs

In connection with the Credit Agreement and the issuance of the Senior Notes, the Company recorded approximately $28.2

million of deferred financing costs. In connection with the increase to the Revolving Credit Facility, the Company recorded an

additional $0.8 million of deferred financing costs. These deferred financing costs are being amortized using the effective

interest method over the estimated life of the related debt. Amortization of the deferred financing costs associated with the

Credit Agreement and the issuance of the Senior Notes included in interest expense for the years ended December 31, 2014,

2013 and 2012 was $2.2 million, $2.7 million and $2.6 million, respectively. Additionally, $2.3 million of deferred issuance

costs were written off in connection with debt retirement for the year ended December 31, 2012 and is reflected in the loss on

extinguishment of debt in the Consolidated Statements of Comprehensive Income.

As of December 31, 2013, $14.0 million of deferred financing costs associated with the Credit Agreement and the issuance

of the Senior Notes was reported as other non-current assets, net in the Consolidated Balance Sheets.

Discount on Debt

The Company recorded a discount on debt from the October 2010 Refinancing of $29.6 million. In connection with

Amendment No. 1, the Company recorded an additional discount of $7.4 million. The discount on debt reflected the difference

between the proceeds received from the issuance of the debt and the face amount to be repaid over the life of the debt. The

discount will be amortized as additional interest expense over the weighted average estimated life of the debt under the

effective interest method. For the years ended December 31, 2014, 2013, and 2012, $2.8 million, $3.5 million and $3.4 million,

respectively, of the discount was amortized as additional interest expense under the effective interest method. Additionally, $2.7

million was written off in connection with debt retirement for the year ended December 31, 2012 and was reflected in the loss

on extinguishment of debt in the Consolidated Statements of Comprehensive Income.

2014 Refinancing of Long-term Debt

On September 30, 2014, the Company repaid the entire outstanding principal balance of $463.6 million of the Credit

Facility; there were no premiums or penalties associated with the repayment. On October 30, 2014, after a required 30-day

notice period, the Company repaid the entire outstanding $760.8 million principal balance of Senior Notes, along with a

required make-whole premium for early repayment of $36.1 million. All of our obligations under the Credit Facility and the

Senior Notes terminated upon the respective repayments thereof.

This transaction was accounted for as an extinguishment of debt under U.S. GAAP. We recognized a loss on debt

extinguishment of $64.9 million for the year ended December 31, 2014, comprised of the $36.1 million make-whole premium

on the Senior Notes and the write-off of the unamortized debt discount and the issuance costs associated with the extinguished

debt of $16.9 million and $11.9 million, respectively.

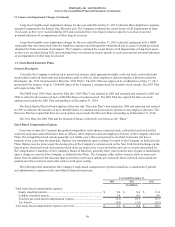

8. Financing Obligations

On May 19, 2008, the Company entered into a Purchase and Sale Agreement relating to the sale and leaseback of 181

parcels of real property (the “Sale-Leaseback Transaction”), each of which is improved with a restaurant operating as an

Applebee's Neighborhood Grill and Bar (the “Properties”). On June 13, 2008, the closing date of the Sale-Leaseback

Transaction, the Company entered into a Master Land and Building Lease (“Master Lease”) for the Properties. The proceeds

received from the transaction were $337.2 million. The Master Lease calls for an initial term of twenty years and four, five-year

options to extend the term.

The Company has an ongoing obligation related to the Properties until such time as the lease related to each of the

Properties is assigned to a qualified franchisee in a transaction meeting certain parameters set forth in the Master Lease. Due to

this continuing involvement, the Sale-Leaseback Transaction was recorded under the financing method in accordance with

U.S. GAAP. Accordingly, the value of the land and leasehold improvements will remain on the Company's books and the

leasehold improvements will continue to be depreciated over their remaining useful lives. The net proceeds received were

recorded as a financing obligation. A portion of the lease payments is recorded as a decrease to the financing obligation and a

portion is recognized as interest expense. In the event the lease obligation of any individual property or group of properties is

assumed by a qualified franchisee, the Company's continuing involvement will cease. At that time, that portion of the

transaction related to that property or group of properties is expected to be recorded as a sale in accordance with U.S. GAAP

and the net book value of those properties will be removed from the Company's books, along with a ratable portion of the

remaining financing obligation.