Harley Davidson 2014 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2014 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

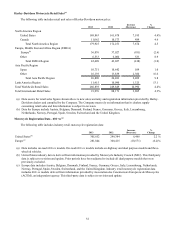

Financial Services Segment

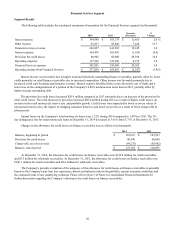

Segment Results

The following table includes the condensed statements of operations for the Financial Services segment (in thousands):€

2014 2013

Increase

(Decrease)

%

Change

Interest income $594,990 $583,174 $11,816 2.0 %

Other income 65,837 58,408 7,429 12.7

Financial services revenue 660,827 641,582 19,245 3.0

Interest expense 164,476 165,491 (1,015)(0.6)

Provision for credit losses 80,946 60,008 20,938 34.9

Operating expenses 137,569 132,990 4,579 3.4

Financial Services expense 382,991 358,489 24,502 6.8

Operating income from Financial Services $277,836 $283,093 $(5,257)(1.9)%

Interest income was favorable due to higher retail and wholesale outstanding finance receivables, partially offset by lower

yields primarily on retail finance receivables due to increased competition. Other income was favorable primarily due to

increased credit card licensing and insurance revenue. Interest expense benefited from a more favorable cost of funds and a

lower loss on the extinguishment of a portion of the Company's 6.80% medium-term notes than in 2013, partially offset by

higher average outstanding debt.

The provision for credit losses increased $20.9 million compared to 2013 primarily due to an increase in the provision for

retail credit losses. The retail motorcycle provision increased $20.0 million during 2014 as a result of higher credit losses, an

increase in the retail motorcycle reserve rate, and portfolio growth. Credit losses were impacted by lower recovery values of

repossessed motorcycles, the impact of changing consumer behavior, and lower recoveries as a result of fewer charge-offs in

prior periods.

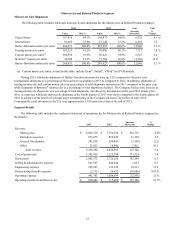

Annual losses on the Company's retail motorcycle loans were 1.22% during 2014 compared to 1.09% in 2013. The 30-

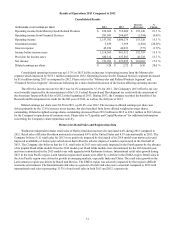

day delinquency rate for retail motorcycle loans at December€31, 2014 decreased to 3.61% from 3.71% at December€31, 2013.

Changes in the allowance for credit losses on finance receivables were as follows (in thousands):€

2014 2013

Balance, beginning of period $110,693 $107,667

Provision for credit losses 80,946 60,008

Charge-offs, net of recoveries (64,275)(56,982)

Balance, end of period $127,364 $110,693

At December€31, 2014, the allowance for credit losses on finance receivables was $122.0 million for retail receivables

and $5.3 million for wholesale receivables. At December€31, 2013, the allowance for credit losses on finance receivables was

$106.1 million for retail receivables and $4.6 million for wholesale receivables.

The Company's periodic evaluation of the adequacy of the allowance for credit losses on finance receivables is generally

based on the Company's past loan loss experience, known and inherent risks in the portfolio, current economic conditions and

the estimated value of any underlying collateral. Please refer to Note 5 of Notes to Consolidated Financial Statements for

further discussion regarding the Company’s allowance for credit losses on finance receivables.

30