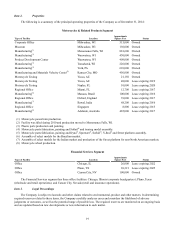

Harley Davidson 2014 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2014 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

historically low levels of retail credit losses during 2013 and 2014, the Company believes HDFS' retail credit losses

may continue to increase over time due to changing consumer credit behavior and HDFS' efforts to increase prudently

structured loan approvals in the sub-prime lending environment. Increases in the frequency of loss and decreases in the

value of repossessed Harley-Davidson branded motorcycles also adversely impact credit losses. If there are adverse

circumstances that involve a material decline in values of Harley-Davidson branded motorcycles, those circumstances

or any related decline in resale values for Harley-Davidson branded motorcycles could contribute to increased

delinquencies and credit losses.

•The Company’s operations may be affected by greenhouse emissions and climate change and related

regulations. Climate change is receiving increasing attention worldwide. Many scientists, legislators and others

attribute climate change to increased levels of greenhouse gases, including carbon dioxide, which has led to significant

legislative and regulatory efforts to limit greenhouse gas emissions. Congress has previously considered and may in

the future implement restrictions on greenhouse gas emissions. In addition, several states, including states where the

Company has manufacturing plants, have previously considered and may in the future implement greenhouse gas

registration and reduction programs. Energy security and availability and its related costs affect all aspects of the

Company’s manufacturing operations in the United States, including the Company’s supply chain. The Company’s

manufacturing plants use energy, including electricity and natural gas, and certain of the Company’s plants emit

amounts of greenhouse gas that may be affected by these legislative and regulatory efforts. Greenhouse gas regulation

could increase the price of the electricity the Company purchases, increase costs for use of natural gas, potentially

restrict access to or the use of natural gas, require the Company to purchase allowances to offset the Company’s own

emissions or result in an overall increase in costs of raw materials, any one of which could increase the Company’s

costs, reduce competitiveness in a global economy or otherwise negatively affect the Company’s business, operations

or financial results. Many of the Company’s suppliers face similar circumstances. Physical risks to the Company’s

business operations as identified by the Intergovernmental Panel on Climate Change and other expert bodies include

scenarios such as sea level rise, extreme weather conditions and resource shortages. Extreme weather may disrupt the

production and supply of component parts or other items such as natural gas, a fuel necessary for the manufacture of

motorcycles and their components. Supply disruptions would raise market rates and jeopardize the continuity of

motorcycle production.

•Regulations related to conflict minerals will cause the Company to incur additional expenses and may have

other adverse consequences. The SEC adopted inquiry, diligence and additional disclosure requirements related to

certain minerals sourced from the Democratic Republic of Congo and surrounding countries, or "conflict minerals",

that are necessary to the functionality of a product manufactured, or contracted to be manufactured, by an SEC

reporting company. The minerals that the rules cover are commonly referred to as "3TG" and include tin, tantalum,

tungsten and gold. These rules impose a requirement for public companies to make certain disclosures relating to

activities with conflict minerals. Compliance with the disclosure requirements could affect the sourcing and

availability of some of the minerals that the Company uses in the manufacturing of its products. The Company's

supply chain is complex, and if it is not able to determine the source and chain of custody for all conflict minerals used

in its products that are sourced from the Democratic Republic of Congo and surrounding countries or determine that

its products are "conflict free", then the Company may face reputational challenges with customers, investors or

others. Additionally, as there may be only a limited number of suppliers offering "conflict free" minerals, if the

Company chooses to use only conflict minerals that are "conflict free", the Company cannot be sure that it will be able

to obtain necessary materials from such suppliers in sufficient quantities or at competitive prices. Accordingly, the

Company could incur significant costs related to the compliance process, including potential difficulty or added costs

in satisfying the disclosure requirements.

The Company disclaims any obligation to update these Risk Factors or any other forward-looking statements. The

Company assumes no obligation (and specifically disclaims any such obligation) to update these Risk Factors or any other

forward-looking statements to reflect actual results, changes in assumptions or other factors affecting such forward-looking

statements.€

18

Item 1B. Unresolved Staff Comments

None.