Harley Davidson 2014 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2014 Harley Davidson annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

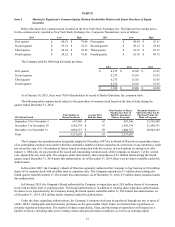

|

|

levels for new motorcycles. Although to a lesser extent than in years prior to the implementation of flexible production, dealers

generally have higher inventory levels of new and used motorcycles in the late fall and winter than during the spring and

summer riding season. As a result, wholesale financing volume is higher during fall and winter as compared to the rest of the

year.

Regulation – The operations of HDFS (both U.S. and foreign) are subject, in certain instances, to supervision and

regulation by state and federal administrative agencies and various foreign governmental authorities. Many of the statutory and

regulatory requirements imposed by such entities are in place to provide consumer protection as it pertains to the selling and

ongoing servicing of financial products and services. Therefore, operations may be subject to various regulations, laws and

judicial and/or administrative decisions imposing requirements and restrictions, which among other things: (a)€regulate credit

granting activities, including establishing licensing requirements, in applicable jurisdictions; (b)€establish maximum interest

rates, finance charges and other charges; (c)€regulate customers’ insurance coverage; (d)€require disclosure of credit and

insurance terms to customers; (e)€govern secured transactions; (f)€set collection, foreclosure, repossession and claims handling

procedures and other trade practices; (g)€prohibit discrimination in the extension of credit and administration of loans;

(h)€regulate the use and reporting of information related to a borrower; (i)€require certain periodic reporting; (j)€govern the use

and protection of non-public personal information; (k)€regulate the use of information reported to the credit reporting agencies;

(l)€regulate the reporting of information to the credit reporting agencies; and/or (m)€regulate insurance solicitation and sales

practices.

Depending on the provisions of the applicable laws and regulations, the interpretation of laws and regulations and the

specific facts and circumstances involved, violations of or non-compliance with these laws may limit the ability of HDFS to

collect all or part of the principal or interest on applicable loans. In addition, these violations or non-compliance may entitle the

borrower to rescind the loan or to obtain a refund of amounts previously paid, could subject HDFS to the payment of damages

or penalties and administrative sanctions, including “cease and desist” orders, and could limit the number of loans eligible for

HDFS securitization programs.

Such regulatory requirements and associated supervision could limit the discretion of HDFS in operating its business.

Noncompliance with applicable statutes or regulations could result in the suspension or revocation of any charter, license or

registration at issue, as well as the imposition of civil fines, criminal penalties and administrative sanctions. The Company

cannot assure that the applicable laws or regulations will not be amended or construed in ways that are adverse to HDFS, that

new laws or regulations will not be adopted in the future, or that laws or regulations will not attempt to limit the interest rates

charged by HDFS, any of which may adversely affect the business of HDFS or its results of operations.

A subsidiary of HDFS, Eaglemark Savings Bank (ESB), is a Nevada state thrift chartered as an Industrial Loan Company

(ILC). As such, the activities of this subsidiary are governed by federal laws and regulations as well as State of Nevada banking

laws, and are subject to examination by the Federal Deposit Insurance Corporation (FDIC) and Nevada state bank examiners.

The Dodd-Frank Wall Street Reform and Consumer Protection Act, which was passed into law in 2010, granted the federal

Consumer Financial Protection Bureau (CFPB) significant supervisory, enforcement, and rule-making authority in the area of

consumer financial products and services. While direct supervision of ESB will remain with the FDIC and the State of Nevada,

certain CFPB regulations, when finalized, will directly impact HDFS and its operations. The CFPB staff recently proposed a

rule that will expand the scope of its supervisory authority to include non-bank larger participants in the vehicle financing

market. This proposed rule was published by the CFPB on October 8, 2014, and if this rule is finalized as proposed, the larger

participant threshold set by the CFPB would include Harley-Davidson Credit Corp. or other Harley-Davidson entities, which

would result in CFBP supervision and periodic examinations of those entities.

ESB originates retail loans and sells the loans to a non-banking subsidiary of HDFS. This process allows HDFS to offer

retail products with many common characteristics across the United States and to similarly service loans to U.S. retail

customers.

Employees – As of December€31, 2014, the Financial Services segment had approximately 600 employees.

11

Item 1A. Risk Factors

An investment in Harley-Davidson, Inc. involves risks, including those discussed below. These risk factors should be

considered carefully before deciding whether to invest in the Company.

•The Company may not be able to successfully execute its long-term business strategy. There is no assurance that

the Company will be able to drive growth to the extent desired through its focus of efforts and resources on its long-

term business strategy and the Harley-Davidson brand or to enhance productivity and profitability to the extent desired

through pricing and continuous improvement.