Frontier Communications 2011 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2011 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

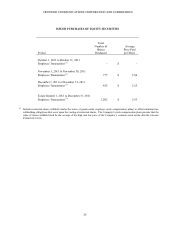

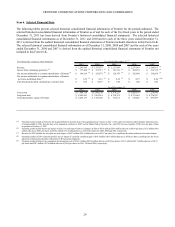

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES

34

aggregate annual rent of approximately $5.8 million. The properties are managed on behalf of the pension plan by an

independent fiduciary, and the terms of the leases were negotiated with the fiduciary on an arm’s-length basis.

In connection with the Transaction, the Company continues to undertake a variety of activities to integrate systems and

implement other initiatives. As a result of the Transaction, the Company incurred $143.1 million of costs related to integration

activities during 2011 as compared to $137.1 million of acquisition and integration costs in 2010. The Company estimates

operating expenses related to its final integration activities in 2012 to be approximately $80 million.

Cash Flows used by Investing Activities

Capital Expenditures

In 2011, 2010 and 2009, our capital expenditures were $824.8 million (including $76.5 million of integration-related capital

expenditures), $577.9 million (including $97.0 million of integration–related capital expenditures) and $256.0 million

(including $25.0 million of integration-related capital expenditures), respectively. Capital expenditures in 2011 and 2010

included $552.5 million and $254.2 million, respectively, associated with the Acquired Business. We continue to closely

scrutinize all of our capital projects, emphasize return on investment and focus our capital expenditures on areas and services

that have the greatest opportunities with respect to revenue growth and cost reduction. We anticipate capital expenditures for

business operations to be approximately $725 million to $775 million for 2012 and capital expenditures for our final

integration activities in 2012 to be approximately $40 million.

Acquisitions

On July 1, 2010, Frontier issued common shares with a value of $5.2 billion and made payments of $105.0 million in cash as

consideration for the Acquired Business. In addition, as part of the Transaction, Frontier assumed approximately $3.5 billion

in debt.

Cash Flows used by and provided from Financing Activities

Bank Financing

On October 14, 2011, the Company entered into a credit agreement (the Credit Agreement) with CoBank, ACB, as

administrative agent, lead arranger and a lender, and the other lenders party thereto for a $575 million senior unsecured term

loan facility with a final maturity of October 14, 2016. Repayment of the outstanding principal balance will be made in

quarterly installments in the amount of $14,375,000, commencing on March 31, 2012, with the remaining outstanding

principal balance to be repaid on the final maturity date. Borrowings under the Credit Agreement bear interest based on the

margins over the Base Rate (as defined in the Credit Agreement) or LIBOR, at the election of the Company. Interest rate

margins under the facility (ranging from 0.875% to 2.875% for Base Rate borrowings and 1.875% to 3.875% for LIBOR

borrowings) are subject to adjustments based on the Total Leverage Ratio of the Company, as such term is defined in the

Credit Agreement. The initial pricing on this facility is LIBOR plus 2.875%, which will vary depending on the leverage ratio,

as described above. The maximum permitted leverage ratio is 4.5 times.

The entire facility was drawn upon execution of the Credit Agreement. Proceeds were used to repay in full the remaining

outstanding principal on three debt facilities (Frontier’s $200 million Rural Telephone Financing Cooperative term loan

maturing October 24, 2011, its $143 million CoBank term loan maturing December 31, 2012, and its $130 million CoBank

term loan maturing December 31, 2013) and the remaining proceeds will be used for general corporate purposes.

The Credit Agreement contains customary representations and warranties, affirmative and negative covenants, including a

restriction on the Company’s ability to declare dividends if an event of default has occurred or will result therefrom, a

financial covenant that requires compliance with a leverage ratio, and customary events of default. Upon proper notice, the

Company may, in whole or in part, repay the facility without premium or penalty, but subject to breakage fees on LIBOR

loans, if applicable. Amounts pre-paid may not be re-borrowed.

Transaction Financing

On April 12, 2010, in anticipation of the Transaction, the Verizon subsidiary then holding the assets of the Acquired Business

completed a private offering of $3.2 billion aggregate principal amount of senior notes. The gross proceeds of the offering,

plus $125.5 million (the Transaction Escrow) contributed by Frontier, were deposited into an escrow account. Immediately

prior to the Transaction, the proceeds of the notes offering (less the initial purchasers’ discount) were released from the

escrow account and used to make a special cash payment to Verizon, as contemplated by the Transaction, with amounts in