Frontier Communications 2011 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2011 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

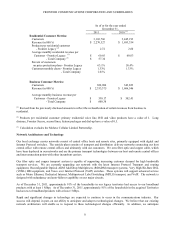

FRONTIER COMMUNICATIONS CORPORATION AND SUBSIDIARIES

18

report certain financial information and adhere for a period of time to certain conditions regulating competition and consumer

protection. The foregoing conditions may restrict our ability to expend cash for other uses and to modify the operations of our

business in response to changing circumstances for a period of time.

Most of the Acquired Business operates on systems acquired from Verizon, which are not as flexible as our

legacy systems.

Currently, certain functions of the Acquired Business in nine states are operated on Verizon replicated information

systems, which are not as flexible as ours and restrict our ability to quickly react to our customers needs. Until such

systems are fully converted, which is currently scheduled to commence in March 2012, our ability to launch new products

and promotions in these acquired Territories on a timely basis may be limited, which may have an adverse impact on our

results of operations.

If the Transaction does not qualify as tax-free under Section 355 of the Internal Revenue Code (the Code),

including as a result of subsequent acquisitions of stock of Frontier, then Verizon or Verizon stockholders may be required

to pay substantial U.S. federal income taxes, and we may be obligated to indemnify Verizon for such taxes imposed on

Verizon or Verizon stockholders.

The Transaction would be taxable to Verizon pursuant to Section 355(e) of the Code if there is a 50% or more

change in ownership of the Acquired Business, directly or indirectly, as part of a plan or series of related transactions that

include the Transaction. Because Verizon stockholders collectively owned more than 50% of the Frontier common stock

following the Transaction, the Transaction alone did not result in a tax to Verizon under Section 355(e). However, Section

355(e) might apply if other acquisitions of stock of Frontier after the Transaction are considered to be part of a plan or

series of related transactions that include the spin-off. If Section 355(e) applies, Verizon might recognize a substantial

amount of taxable gain and we may be liable to indemnify Verizon.

Under a tax sharing agreement, in certain circumstances, and subject to certain limitations, we are required to

indemnify Verizon against taxes on the Transaction that arise as a result of actions or failures to act by us, or as a result of

changes in ownership of our stock after the Transaction. See “We will be unable to take certain actions until July 2012

because such actions could jeopardize the tax-free status of the Transaction, and such restrictions could be significant.”

We will be unable to take certain actions until July 2012 because such actions could jeopardize the tax-free

status of the Transaction, and such restrictions could be significant.

The tax sharing agreement prohibits us from taking actions that could reasonably be expected to cause the

Transaction to be taxable or to jeopardize the conclusions of the IRS ruling or opinions of counsel received by Verizon or

Frontier. In particular, for two years after the spin-off, or until July 2012, we may not:

• enter into any agreement, understanding or arrangement or engage in any substantial negotiations with

respect to any transaction involving the acquisition, issuance, repurchase or change of ownership of

Frontier capital stock, or options or other rights in respect of Frontier capital stock, subject to certain

exceptions relating to employee compensation arrangements, stock splits, open market stock repurchases

and stockholder rights plans;

• permit certain wholly owned subsidiaries owned by the Acquired Business at the time of the Transaction

to cease the active conduct of the Acquired Business to the extent it was conducted immediately prior to

the Transaction; or

• voluntarily dissolve, liquidate, merge or consolidate with any other person, unless we survive and the

transaction otherwise complies with the restrictions in the tax sharing agreement.

Nevertheless, we will be permitted to take any of the actions described above if we obtain Verizon’s consent, or if

we obtain a supplemental IRS private letter ruling (or an opinion of counsel that is reasonably acceptable to Verizon) to the

effect that the action will not affect the tax-free status of the Transaction. However, the receipt of any such consent,

opinion or ruling does not relieve us of any obligation we have to indemnify Verizon for an action we take that causes the

Transaction to be taxable to Verizon.