Dollar General 2014 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2014 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

10-K

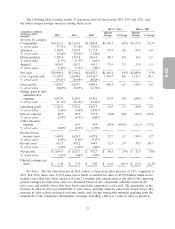

capital outlays for leasehold improvements, fixtures and equipment; the construction of new stores;

costs to support and enhance our supply chain initiatives including the distribution center under

construction in Texas; technology initiatives; as well as routine and ongoing capital requirements.

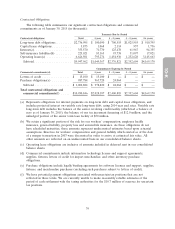

Cash flows from financing activities. In 2014, we repurchased 14.1 million outstanding shares of

our common stock at a total cost of $800.1 million. We made repayments of $75.0 million on the

balance of the Term Facility. Borrowings and repayments under the Revolving Facility during the 2014

period were the same amount, resulting in no net increase to amounts outstanding under the Revolving

Facility during 2014.

The 2013 cash flows from financing activities reflect our refinancing in April 2013, including the

issuance of long-term obligations which includes the $1.0 billion unsecured Term Facility and the

issuance of Senior Notes totaling approximately $1.3 billion. Proceeds from these transactions were

used to extinguish our previous secured term loan and revolving credit facilities which had balances of

$1.96 billion and $155.6 million at termination. Net repayments under the Revolving Facility were

$130.9 million during 2013. We paid debt issuance costs and hedging fees totaling $29.2 million in 2013

related to the refinancing. Also in 2013, we repurchased 11.0 million outstanding shares of our common

stock at a total cost of $620.1 million.

In 2012 we repurchased 14.4 million outstanding shares of our common stock at a total cost of

$671.4 million. In July 2012, we issued $500.0 million aggregate principal amount of 4.125% senior

notes due 2017. Also in July 2012, we redeemed the remaining aggregate principal amount of senior

subordinated notes due 2017 at a redemption price of 105.938% of the principal amount thereof,

resulting in a cash outflow of $477.5 million. Net borrowings under our senior secured revolving credit

facility were $101.8 million during 2012.

Critical Accounting Policies and Estimates

The preparation of financial statements in accordance with U.S. GAAP requires management to

make estimates and assumptions that affect reported amounts and related disclosures. In addition to

the estimates presented below, there are other items within our financial statements that require

estimation, but are not deemed critical as defined below. We believe these estimates are reasonable and

appropriate. However, if actual experience differs from the assumptions and other considerations used,

the resulting changes could have a material effect on the financial statements taken as a whole.

Management believes the following policies and estimates are critical because they involve

significant judgments, assumptions, and estimates. Management has discussed the development and

selection of the critical accounting estimates with the Audit Committee of our Board of Directors, and

the Audit Committee has reviewed the disclosures presented below relating to those policies and

estimates. See Note 1 to the consolidated financial statements for a detailed discussion of our principal

accounting policies.

Merchandise Inventories. Merchandise inventories are stated at the lower of cost or market

(‘‘LCM’’) with cost determined using the retail last in, first out (‘‘LIFO’’) method. We use the retail

inventory method (‘‘RIM’’) to calculate gross profit and the resulting valuation of inventories at cost,

which are computed by applying a calculated cost-to-retail inventory ratio to the retail value of sales at

a department level. The RIM is an averaging method that has been widely used in the retail industry

due to its practicality. Also, the use of the RIM will result in valuing inventories at LCM if markdowns

are currently taken as a reduction of the retail value of inventories. Inherent in the retail inventory

method calculation are certain significant management judgments and estimates including, among

others, initial markups, markdowns, and shrinkage, which significantly impact the gross profit

calculation as well as the ending inventory valuation at cost. These significant estimates, coupled with

42