Delta Airlines 2005 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2005 Delta Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

Table of Contents

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

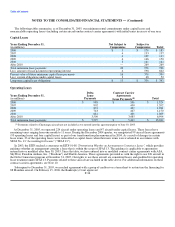

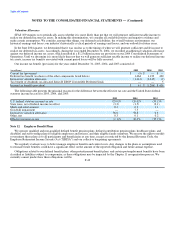

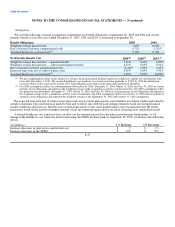

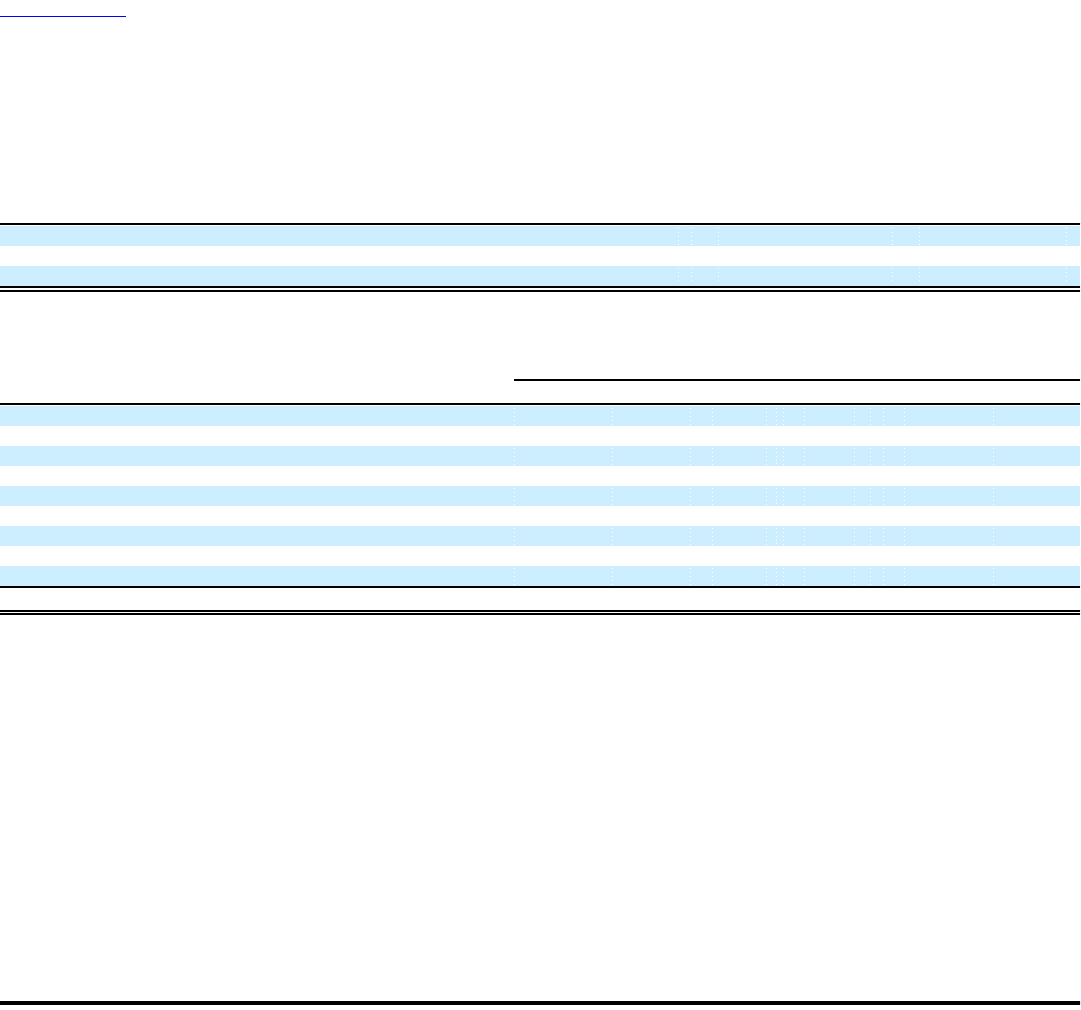

The accumulated benefit obligation for all our defined benefit pension plans was $12.8 billion and $12.1 billion at December 31,

2005 and 2004, respectively. The following table contains information about our pension plans with an accumulated benefit obligation

in excess of plan assets (measured at September 30):

(in millions) 2005 2004

Projected benefit obligation $ 12,893 $ 12,140

Accumulated benefit obligation 12,844 12,081

Fair value of plan assets 6,521 6,842

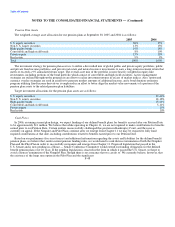

Net periodic benefit cost for the years ended December 31, 2005, 2004 and 2003, included the following components:

Pension Other

Benefits Postretirement Benefits

(in millions) 2005 2004 2003 2005 2004 2003

Service cost $ 155 $ 233 $ 238 $ 17 $ 28 $ 33

Interest cost 715 757 768 114 121 161

Expected return on plan assets (598) (657) (753) — — —

Amortization of prior service cost (benefit) 3 15 13 (41) (79) (47)

Recognized net actuarial loss 179 194 97 13 6 7

Amortization of net transition obligation 6 7 7 — — —

Settlement charge 388 257 219 — — —

Curtailment loss (gain) 434 — 47 — (527) (4)

Special termination benefits — 10 — — 142 —

Net periodic benefit cost $ 1,282 $ 816 $ 636 $ 103 $ (309) $ 150

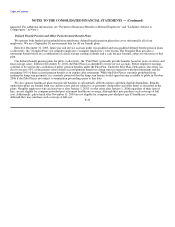

During 2005, 2004, and 2003, we recorded settlement charges totaling $388 million, $257 million, and $219 million, respectively,

in our Consolidated Statements of Operations. These charges primarily relate to the Pilot Plan and result from lump sum distributions

to pilots who retired. We recorded these charges in accordance with SFAS No. 88, "Employers' Accounting for Settlements and

Curtailments of Defined Benefit Pension Plans and for Termination Benefits" ("SFAS 88"). SFAS 88 requires settlement accounting if

the cost of all settlements, including lump sum retirement benefits paid, in a year exceeds, or is expected to exceed, the total of the

service and interest cost components of pension expense for the same period.

During 2005 and 2004, we recorded a net curtailment loss of $434 million and a curtailment gain of $527 million, respectively, in

our Consolidated Statements of Operations. The $434 million net curtailment loss consists of (1) a $13 million curtailment gain

recorded in the December 2005 quarter related to the freeze of benefit accruals effective December 31, 2005 for the Nonpilot Plan and

(2) a curtailment loss of $447 million related to the impact of the reduction of nonpilot jobs announced in November 2004 and the

freeze of service accruals under the Pilot Plan effective December 31, 2004. Additionally, in the December 2004 quarter, we recorded

a $527 million curtailment gain related to the elimination of company subsidized retiree medical benefits for eligible employees who

retire after January 1, 2006. These losses and gains are in accordance with SFAS 88, which requires curtailment accounting when an

event occurs that significantly reduces the expected years of future service of current employees or that eliminates future benefit

accruals for a significant number of employees. F-46