DIRECTV 2008 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2008 DIRECTV annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142

|

|

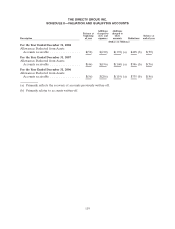

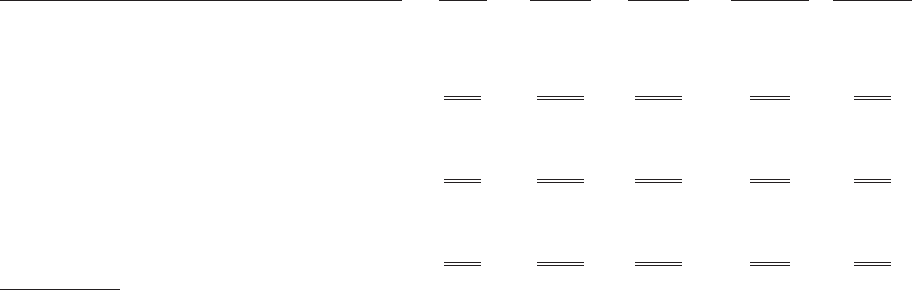

THE DIRECTV GROUP, INC.

SCHEDULE II—VALUATION AND QUALIFYING ACCOUNTS

Additions Additions

Balance at charged to charged to

beginning costs and other Balance at

Description of year expenses accounts Deductions end of year

(Dollars in Millions)

For the Year Ended December 31, 2008

Allowances Deducted from Assets

Accounts receivable ................. $(56) $(210) $(192) (a) $408 (b) $(50)

For the Year Ended December 31, 2007

Allowances Deducted from Assets

Accounts receivable ................. $(46) $(196) $(160) (a) $346 (b) $(56)

For the Year Ended December 31, 2006

Allowances Deducted from Assets

Accounts receivable ................. $(56) $(206) $(119) (a) $335 (b) $(46)

(a) Primarily reflects the recovery of accounts previously written-off.

(b) Primarily relates to accounts written-off.

119