DIRECTV 2008 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2008 DIRECTV annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

THE DIRECTV GROUP, INC.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS—(continued)

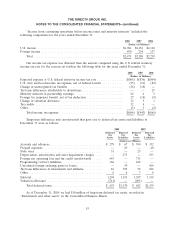

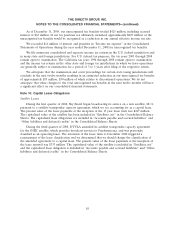

Net periodic pension benefit costs for 2007 includes one month of expense that was recorded as an

adjustment to ‘‘Accumulated deficit’’ in the Consolidated Balance Sheets ($1 million after tax) related

to the adoption of the measurement date provisions of SFAS No. 158 discussed in Note 2.

Assumptions

Weighted-average assumptions used to determine benefit obligations at December 31:

Other

Pension Postretirement

Benefits Benefits

2008 2007 2008 2007

Discount rate—Qualified Plans ............................... 6.06% 6.22% 5.88% 5.76%

Discount rate—Non-Qualified Plans ........................... 6.04% 6.24% — —

Rate of compensation increase ............................... 4.00% 4.00% 4.00% 4.00%

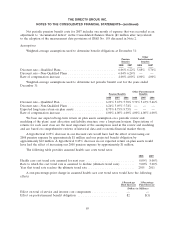

Weighted-average assumptions used to determine net periodic benefit cost for the years ended

December 31:

Other Postretirement

Pension Benefits Benefits

2008 2007 2006 2008 2007 2006

Discount rate—Qualified Plan ........................ 6.22% 5.67% 5.78% 5.76% 5.43% 5.46%

Discount rate—Non-Qualified Plans .................... 6.24% 5.69% 5.74% — — —

Expected long-term return on plan assets ................ 8.75% 8.75% 8.75% — — —

Rate of compensation increase ........................ 4.00% 4.00% 4.00% 4.00% 4.00% 4.00%

We base our expected long-term return on plan assets assumption on a periodic review and

modeling of the plans’ asset allocation and liability structure over a long-term horizon. Expectations of

returns for each asset class are the most important of the assumptions used in the review and modeling

and are based on comprehensive reviews of historical data and economic/financial market theory.

A hypothetical 0.25% decrease in our discount rate would have had the effect of increasing our

2008 pension expense by approximately $1 million and our projected benefit obligation by

approximately $12 million. A hypothetical 0.25% decrease in our expected return on plan assets would

have had the effect of increasing our 2008 pension expense by approximately $1 million.

The following table provides assumed health care costs trend rates:

2008 2007

Health care cost trend rate assumed for next year ............................ 8.00% 8.00%

Rate to which the cost trend rate is assumed to decline (ultimate trend rate) ........ 5.00% 5.00%

Year that trend rate reaches the ultimate trend rate ........................... 2015 2011

A one-percentage-point change in assumed health care cost trend rates would have the following

effects:

1-Percentage 1-Percentage

Point Increase Point Decrease

(Dollars in Millions)

Effect on total of service and interest cost components ............... — —

Effect on postretirement benefit obligation ....................... $2 $(1)

89