Cisco 2015 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2015 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

The goodwill recorded in the Consolidated Balance Sheets as of July 25, 2015 and July 26, 2014 was $24.5 billion and $24.2 billion,

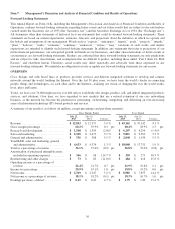

respectively. In response to changes in industry and market conditions, we could be required to strategically realign our resources

and consider restructuring, disposing of, or otherwise exiting businesses, which could result in an impairment of goodwill. There was

no impairment of goodwill resulting from our annual impairment testing in fiscal 2015, 2014, and 2013. For the annual impairment

testing in fiscal 2015, the excess of the fair value over the carrying value for each of our reporting units was $40.8 billion for the

Americas, $32.6 billion for EMEA, and $12.9 billion for APJC. During the fourth quarter of fiscal 2015, we performed a sensitivity

analysis for goodwill impairment with respect to each of our respective reporting units and determined that a hypothetical 10%

decline in the fair value of each reporting unit would not result in an impairment of goodwill for any reporting unit.

We make judgments about the recoverability of purchased intangible assets with finite lives whenever events or changes in

circumstances indicate that an impairment may exist. Recoverability of purchased intangible assets with finite lives is measured by

comparing the carrying amount of the asset to the future undiscounted cash flows the asset is expected to generate. We review

indefinite-lived intangible assets for impairment annually or whenever events or changes in circumstances indicate that the asset

might be impaired. If the asset is considered to be impaired, the amount of any impairment is measured as the difference between the

carrying value and the fair value of the impaired asset. Assumptions and estimates about future values and remaining useful lives of

our purchased intangible assets are complex and subjective. They can be affected by a variety of factors, including external factors

such as industry and economic trends, and internal factors such as changes in our business strategy and our internal forecasts. Our

impairment charges related to purchased intangible assets were $175 million during fiscal 2015. There were no impairment charges

related to purchased intangible assets during fiscal 2014 and fiscal 2013. Our ongoing consideration of all the factors described

previously could result in additional impairment charges in the future, which could adversely affect our net income.

Income Taxes

We are subject to income taxes in the United States and numerous foreign jurisdictions. Our effective tax rates differ from the

statutory rate, primarily due to the tax impact of state taxes, foreign operations, R&D tax credits, domestic manufacturing

deductions, tax audit settlements, nondeductible compensation, international realignments, and transfer pricing adjustments. Our

effective tax rate was 19.8%, 19.2%, and 11.1% in fiscal 2015, 2014, and 2013, respectively.

Significant judgment is required in evaluating our uncertain tax positions and determining our provision for income taxes.

Although we believe our reserves are reasonable, no assurance can be given that the final tax outcome of these matters will not be

different from that which is reflected in our historical income tax provisions and accruals. We adjust these reserves in light of

changing facts and circumstances, such as the closing of a tax audit or the refinement of an estimate. To the extent that the final

tax outcome of these matters is different than the amounts recorded, such differences will impact the provision for income taxes

in the period in which such determination is made. The provision for income taxes includes the impact of reserve provisions and

changes to reserves that are considered appropriate, as well as the related net interest and penalties.

Significant judgment is also required in determining any valuation allowance recorded against deferred tax assets. In assessing

the need for a valuation allowance, we consider all available evidence, including past operating results, estimates of future taxable

income, and the feasibility of tax planning strategies. In the event that we change our determination as to the amount of deferred

tax assets that can be realized, we will adjust our valuation allowance with a corresponding impact to the provision for income

taxes in the period in which such determination is made.

Our provision for income taxes is subject to volatility and could be adversely impacted by earnings being lower than anticipated

in countries that have lower tax rates and higher than anticipated in countries that have higher tax rates; by changes in the

valuation of our deferred tax assets and liabilities; by expiration of or lapses in the R&D tax credit or domestic manufacturing

deduction laws; by expiration of or lapses in tax incentives; by transfer pricing adjustments, including the effect of acquisitions

on our intercompany R&D cost-sharing arrangement and legal structure; by tax effects of nondeductible compensation; by tax

costs related to intercompany realignments; by changes in accounting principles; or by changes in tax laws and regulations,

treaties, or interpretations thereof, including possible changes to the taxation of earnings of our foreign subsidiaries, the

deductibility of expenses attributable to foreign income, or the foreign tax credit rules. Significant judgment is required to

determine the recognition and measurement attributes prescribed in the accounting guidance for uncertainty in income taxes. The

Organisation for Economic Co-operation and Development (OECD), an international association comprised of 34 countries,

including the United States, is contemplating changes to numerous long-standing tax principles. These contemplated changes, if

finalized and adopted by countries, will increase tax uncertainty and may adversely affect our provision for income taxes. As a

result of certain of our ongoing employment and capital investment actions and commitments, our income in certain countries is

subject to reduced tax rates and in some cases is wholly exempt from tax. Our failure to meet these commitments could adversely

impact our provision for income taxes. In addition, we are subject to the continuous examination of our income tax returns by the

Internal Revenue Service (IRS) and other tax authorities. We regularly assess the likelihood of adverse outcomes resulting from

these examinations to determine the adequacy of our provision for income taxes. There can be no assurance that the outcomes

from these continuous examinations will not have an adverse impact on our operating results and financial condition.

43