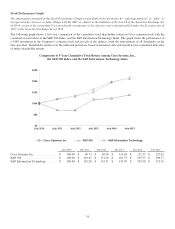

Cisco 2015 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2015 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

We make sales to distributors which we refer to as two-tier systems of sales to the end customer. Revenue from distributors is

recognized based on a sell-through method using information provided by them. Our distributors participate in various

cooperative marketing and other programs, and we maintain estimated accruals and allowances for these programs. If actual

credits received by our distributors under these programs were to deviate significantly from our estimates, which are based on

historical experience, our revenue could be adversely affected.

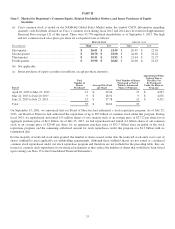

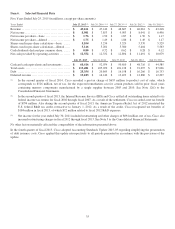

Allowances for Receivables and Sales Returns

The allowances for receivables were as follows (in millions, except percentages):

July 25, 2015 July 26, 2014

Allowance for doubtful accounts ........................................................ $ 302 $ 265

Percentage of gross accounts receivable ................................................ 5.4% 4.9%

Allowance for credit loss—lease receivables ............................................ $ 259 $ 233

Percentage of gross lease receivables (1) ................................................ 7.2% 6.2%

Allowance for credit loss—loan receivables ............................................. $87$98

Percentage of gross loan receivables .................................................... 4.9% 5.8%

(1) Calculated as allowance for credit loss on lease receivables as a percentage of gross lease receivables and residual value before unearned

income.

The allowance for doubtful accounts is based on our assessment of the collectibility of customer accounts. We regularly review

the adequacy of these allowances by considering internal factors such as historical experience, credit quality and age of the

receivable balances as well as external factors such as economic conditions that may affect a customer’s ability to pay and

expected default frequency rates, which are published by major third-party credit-rating agencies and are generally updated on a

quarterly basis. We also consider the concentration of receivables outstanding with a particular customer in assessing the

adequacy of our allowances for doubtful accounts. If a major customer’s creditworthiness deteriorates, if actual defaults are

higher than our historical experience, or if other circumstances arise, our estimates of the recoverability of amounts due to us

could be overstated, and additional allowances could be required, which could have an adverse impact on our operating results.

The allowance for credit loss on financing receivables is also based on the assessment of collectibility of customer accounts. We

regularly review the adequacy of the credit allowances determined either on an individual or a collective basis. When evaluating

the financing receivables on an individual basis, we consider historical experience, credit quality and age of receivable balances,

and economic conditions that may affect a customer’s ability to pay. When evaluating financing receivables on a collective basis,

we use expected default frequency rates published by a major third-party credit-rating agency as well as our own historical loss

rate in the event of default, while also systematically giving effect to economic conditions, concentration of risk and correlation.

Determining expected default frequency rates and loss factors associated with internal credit risk ratings, as well as assessing

factors such as economic conditions, concentration of risk, and correlation, are complex and subjective. Our ongoing

consideration of all these factors could result in an increase in our allowance for credit loss in the future, which could adversely

affect our operating results. Both accounts receivable and financing receivables are charged off at the point when they are

considered uncollectible.

A reserve for future sales returns is established based on historical trends in product return rates. The reserve for future sales

returns as of July 25, 2015 and July 26, 2014 was $129 million and $135 million, respectively, and was recorded as a reduction of

our accounts receivable. If the actual future returns were to deviate from the historical data on which the reserve had been

established, our revenue could be adversely affected.

Inventory Valuation and Liability for Purchase Commitments with Contract Manufacturers and Suppliers

Our inventory balance was $1.6 billion as of each July 25, 2015 and July 26, 2014. Inventory is written down based on excess and

obsolete inventories, determined primarily by future demand forecasts. Inventory write-downs are measured as the difference

between the cost of the inventory and market, based upon assumptions about future demand, and are charged to the provision for

inventory, which is a component of our cost of sales. At the point of the loss recognition, a new, lower cost basis for that

inventory is established, and subsequent changes in facts and circumstances do not result in the restoration or increase in that

newly established cost basis.

We record a liability for firm, noncancelable, and unconditional purchase commitments with contract manufacturers and suppliers

for quantities in excess of our future demand forecasts consistent with the valuation of our excess and obsolete inventory. As of

July 25, 2015, the liability for these purchase commitments was $156 million, compared with $162 million as of July 26, 2014,

and was included in other current liabilities.

40