Cisco 2008 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2008 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

2008 Annual Report 37

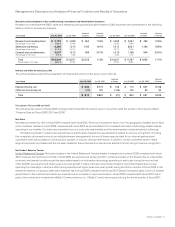

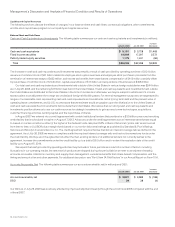

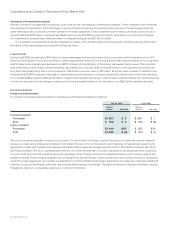

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Recent Accounting Pronouncements and Developments

SFAS 157 In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (“SFAS 157”). SFAS 157 defines fair value,

establishes a framework for measuring fair value, and enhances fair value measurement disclosure. In February 2008, the FASB issued

FASB Staff Position (“FSP”) 157-1, “Application of FASB Statement No. 157 to FASB Statement No. 13 and Other Accounting Pronouncements

That Address Fair Value Measurements for Purposes of Lease Classification or Measurement under Statement 13” (“FSP 157-1”) and

FSP 157-2, “Effective Date of FASB Statement No. 157” (“FSP 157-2”). FSP 157-1 amends SFAS 157 to remove certain leasing transactions

from its scope. FSP 157-2 delays the effective date of SFAS 157 for all nonfinancial assets and nonfinancial liabilities, except for items that

are recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually), until the beginning of the first

quarter of fiscal 2010. The measurement and disclosure requirements related to financial assets and financial liabilities are effective for us in

the first quarter of fiscal 2009. The adoption of SFAS 157 for financial assets and financial liabilities is not expected to have a material impact

on our results of operations or financial position. We are currently assessing the impact that SFAS 157 will have on our results of operations

and financial position when it is applied to nonfinancial assets and nonfinancial liabilities beginning in the first quarter of fiscal 2010.

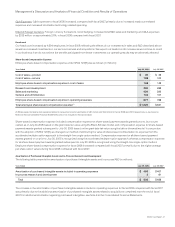

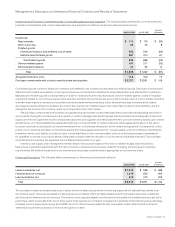

SFAS 159 In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities—Including

an amendment of FASB Statement No. 115” (“SFAS 159”). SFAS 159 is expected to expand the use of fair value accounting but does not

affect existing standards that require certain assets or liabilities to be carried at fair value. The objective of SFAS 159 is to improve financial

reporting by providing companies with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and

liabilities differently without having to apply complex hedge accounting provisions. Under SFAS 159, a company may choose, at specified

election dates, to measure eligible items at fair value and report unrealized gains and losses on items for which the fair value option has

been elected in earnings at each subsequent reporting date. SFAS 159 is effective for us in the first quarter of fiscal 2009, and it is not

expected to have a material impact on our results of operations or financial position.

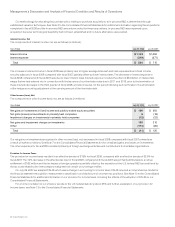

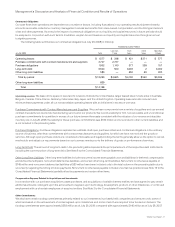

SFAS 141(R) and SFAS 160 In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“SFAS 141(R)”) and

SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements—an amendment of ARB No. 51” (“SFAS 160”). SFAS 141(R)

will significantly change current practices regarding business combinations. Among the more significant changes, SFAS 141(R) expands

the definition of a business and a business combination; requires the acquirer to recognize the assets acquired, liabilities assumed and

noncontrolling interests (including goodwill), measured at fair value at the acquisition date; requires acquisition-related expenses and

restructuring costs to be recognized separately from the business combination; requires assets acquired and liabilities assumed from

contractual and noncontractual contingencies to be recognized at their acquisition-date fair values with subsequent changes recognized

in earnings; and requires in-process research and development to be capitalized at fair value as an indefinite-lived intangible asset.

SFAS 160 will change the accounting and reporting for minority interests, reporting them as equity separate from the parent entity’s

equity, as well as requiring expanded disclosures. SFAS 141(R) and SFAS 160 are effective for financial statements issued for fiscal years

beginning after December 15, 2008. We are currently assessing the impact that SFAS 141(R) and SFAS 160 will have on our results of

operations and financial position.

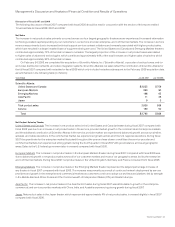

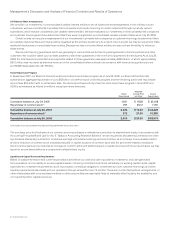

SFAS 161 In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities, an amendment

of FASB Statement No. 133” (“SFAS 161”), which requires additional disclosures about the objectives of using derivative instruments; the

method by which the derivative instruments and related hedged items are accounted for under FASB Statement No.133 and its related

interpretations; and the effect of derivative instruments and related hedged items on financial position, financial performance, and cash

flows. SFAS 161 also requires disclosure of the fair values of derivative instruments and their gains and losses in a tabular format.

SFAS 161 is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008, with early

adoption encouraged. We are currently assessing the impact that the adoption of SFAS 161 will have on our financial statement disclosures.

IFRS On August 27, 2008, the U.S. Securities and Exchange Commission (SEC) announced that they will issue for comment a proposed

roadmap regarding the potential use by U.S. issuers of financial statements prepared in accordance with International Financial Reporting

Standards (IFRS). IFRS is a comprehensive series of accounting standards published by the International Accounting Standards Board

(IASB). Under the proposed roadmap, we could be required in fiscal 2014 to prepare financial statements in accordance with IFRS, and

the SEC will make a determination in 2011 regarding the mandatory adoption of IFRS. We are currently assessing the impact that this

potential change would have on our consolidated financial statements, and we will continue to monitor the development of the potential

implementation of IFRS.