Advance Auto Parts 2005 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2005 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

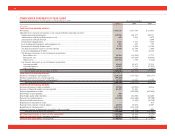

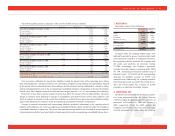

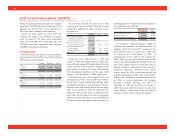

The fair value of each stock option was estimated

on the date of the grant using the Black-Scholes

option-pricing model with the following weighted

average assumptions:

2005 2004 2003

Risk-free interest rate ............... 3.7% 3.3% 3.1%

Expected dividend yield........... ———

Expected stock price volatility.. 33.2% 34.3% 41.0%

Expected life of stock options.. 4 years 4 years 4 years

The weighted average fair value of stock options

granted during fiscal 2005, 2004 and 2003 used in

computing pro forma compensation expense was

$10.54, $8.28 and $5.07 per share, respectively.

Goodwill and Other Intangible Assets

In accordance with SFAS No. 142, “Goodwill and

Other Intangible Assets,” the Company tests goodwill

for impairment at least on an annual basis. Testing for

impairment is a two-step process as prescribed in

SFAS No. 142. The first step is a review for potential

impairment, while the second step measures the

amount of impairment, if any. Under the guidelines

of SFAS No. 142, the Company is required to per-

form an impairment test at least on an annual basis at

any time during the fiscal year provided the test is

performed at the same time every year. The Company

has elected to complete its annual impairment test as

of the end of its third quarter. An impairment loss

would be recognized when the assets’ fair value is

below their carrying value.

Valuation of Long-Lived Assets

The Company evaluates the recoverability of its

long-lived assets under the provisions of SFAS No.

144, “Accounting for the Impairment or Disposal of

Long-Lived Assets.” SFAS No. 144 requires the

review for impairment of long-lived assets, whenever

events or changes in circumstances indicate that the

carrying amount of an asset might not be recoverable

and exceeds its fair value.

Significant factors, which would trigger an impair-

ment review, include the following:

• Significant negative industry trends;

• Significant changes in technology;

• Significant underutilization of assets; and

• Significant changes in how assets are used or are

planned to be used.

When such an event occurs, the Company esti-

mates the future cash flows expected to result from

the use of the asset and its eventual disposition. These

impairment evaluations involve estimates of asset

useful lives and future cash flows. If the undiscount-

ed expected future cash flows are less than the carry-

ing amount of the asset and the carrying amount of

the asset exceeds its fair value, an impairment loss is

recognized. Management utilizes an expected present

value technique, which uses a risk-free rate and mul-

tiple cash flow scenarios reflecting the range of pos-

sible outcomes, to estimate fair value of the asset.

Actual useful lives and cash flows could differ from

those estimated by management using these tech-

niques, which could have a material affect on our

results of operations, financial position or liquidity.

There were no reductions to the carrying amounts

currently assigned to the Company’s long-lived assets

during fiscal years 2005, 2004 and 2003, respectively.

Financed Vendor Accounts Payable

In fiscal 2004, the Company entered a short-term

financing program with a bank allowing it to extend

its payment terms on certain merchandise purchases.

The substance of the program is for the Company to

borrow money from the bank to finance purchases

from vendors. The Company records any discount

given by the vendor to the value of its inventory and

accretes this discount to the resulting short-term

payable to the bank through interest expense over the

extended term. At December 31, 2005 and January 1,

2005, $119,351 and $56,896, respectively, was

payable to the bank by the Company under this pro-

gram and is included in the accompanying condensed

consolidated balance sheets as Financed Vendor

Accounts Payable.

Lease Accounting

The Company leases certain store locations, distri-

bution centers, office space, equipment and vehicles,

some of which are with related parties. Initial terms

for facility leases are typically 10 to 15 years, fol-

lowed by additional terms containing renewal options

at five year intervals, and may include rent escalation

clauses. The total amount of the minimum rent is

expensed on a straight-line basis over the initial term

of the lease unless external economic factors exist

such that renewals are reasonably assured, in which

case the Company would include the renewal period

in its amortization period. In those instances the

renewal period would be included in the lease term

for purposes of establishing an amortization period

and determining if such lease qualified as a capital or

operating lease. In addition to minimum fixed

rentals, some leases provide for contingent facility

rentals. Contingent facility rentals are determined on

the basis of a percentage of sales in excess of stipu-

lated minimums for certain store facilities as defined

in the individual lease agreements. Most of the leas-

es provide that the Company pay taxes, maintenance,

insurance and certain other expenses applicable to the

42

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(continued)

For the Years Ended December 31, 2005, January 1, 2005 and January 3, 2004 (in thousands, except per share data)