Advance Auto Parts 2005 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2005 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

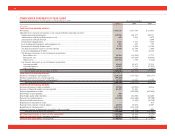

The senior credit facility is secured by a first priority

lien on substantially all of our assets and the assets of

our existing domestic subsidiaries, subject to certain

exceptions, and will be secured by the properties and

assets of our future domestic subsidiaries. The senior

credit facility contains covenants restricting the ability

of us and our subsidiaries to, among other things, (1)

declare dividends or redeem or repurchase capital

stock, (2) prepay, redeem or purchase debt, (3) incur

liens or engage in sale-leaseback transactions, (4)

make loans and investments, (5) incur additional debt

(including hedging arrangements), (6) engage in certain

mergers, acquisitions and asset sales, (7) engage in

transactions with affiliates, (8) change the nature of

our business and the business conducted by our sub-

sidiaries and (9) change our passive holding company

status. We also are required to comply with financial

covenants with respect to a maximum leverage ratio,

a minimum interest coverage ratio, a minimum cur-

rent assets to funded senior debt ratio, a maximum

senior leverage ratio and limits on capital expendi-

tures. We were in compliance with the above

covenants at December 31, 2005.

CREDIT RATINGS

At December 31, 2005, we had a credit rating on

our senior credit facility from Standard & Poor’s of

BB+ and a credit rating of Ba1 from Moody’s

Investor Service. The current pricing grid used to

determine our borrowing rates under our senior cred-

it facility is based on such credit ratings. If these

credit ratings decline, our interest expense may

increase. Conversely, if these credit ratings increase,

our interest expense may decrease.

SEASONALITY

Our business is somewhat seasonal in nature, with

the highest sales occurring in the spring and summer

months. In addition, our business can be affected by

weather conditions. While unusually heavy precipi-

tation tends to soften sales as elective maintenance is

deferred during such periods, extremely hot or cold

weather tends to enhance sales by causing automo-

tive parts to fail at an accelerated rate.

RECENT ACCOUNTING PRONOUNCEMENTS

In November 2004 the FASB issued SFAS No.

151, “Inventory Costs.” The new statement amends

Accounting Research Bulletin No. 43, Chapter 4,

“Inventory Pricing,” to clarify the accounting for

abnormal amounts of idle facility expense, freight,

handling costs and wasted material. This statement

requires that those items be recognized as current-

period charges and requires that allocation of fixed

production overheads to the cost of conversion be

based on the normal capacity of the production facil-

ities. This statement is effective for fiscal years

beginning after June 15, 2005. We do not expect the

adoption of this statement to have a material impact

on our financial condition, results of operations or

cash flows.

In December 2004 the FASB issued SFAS No. 123

(revised 2004), “Share-Based Payment,” or SFAS

No. 123R. SFAS No. 123R replaces SFAS No. 123

and supersedes APB Opinion No. 25 and subse-

quently issued stock option related guidance. SFAS

No. 123R establishes standards for the accounting

for transactions in which an entity exchanges its

equity instruments for goods or services, primarily

on accounting for transactions in which an entity

obtains employee services in share-based payment

transactions. It also addresses transactions in which

an entity incurs liabilities in exchange for goods or

services that are based on the fair value of the enti-

ty’s equity instruments or that may be settled by the

issuance of those equity instruments. Entities will be

required to measure the cost of employee services

received in exchange for an award of equity instru-

ments based on the grant-date fair value of the award

(with limited exceptions). That cost will be recog-

nized over the period during which an employee is

required to provide service in exchange for the award

(usually the vesting period). The grant-date fair

value of employee share options and similar instru-

ments will be estimated using option-pricing mod-

els. If an equity award is modified after the grant

date, incremental compensation cost will be recog-

nized in an amount equal to the excess of the fair

value of the modified award over the fair value of the

original award immediately before the modification.

We are required to apply SFAS No. 123R to all

stock or stock-based awards outstanding and subse-

quently granted, modified or settled as of January 1,

2006. SFAS No. 123R requires us to use either the

modified-prospective method or modified-retro-

spective method. Under the modified-prospective

method, we must recognize compensation cost for all

awards subsequent to adopting the standard and for

the unvested portion of previously granted awards

outstanding upon adoption. Under the modified-ret-

rospective method, we must restate our previously

issued financial statements to recognize the amounts

we previously calculated and reported on a pro

forma basis, as if the prior standard had been adopt-

ed. Under both methods, SFAS No. 123R permits the

use of either the straight line or an accelerated

32

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(continued)