ADT 2014 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2014 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

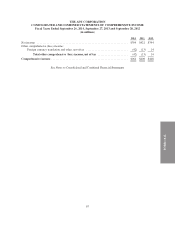

FORM 10-K

of Other Comprehensive Income (“OCI”) by eliminating the option to present OCI as part of the statement of

stockholders’ equity. The amendment does not impact the accounting for OCI, but does impact its presentation in

the Company’s Consolidated and Combined Financial Statements. The guidance requires that items of net

income and OCI be presented either in a single continuous statement of comprehensive income or in two separate

but consecutive statements which include total net income and its components, consecutively followed by total

OCI and its components to arrive at total comprehensive income. In December 2011, the FASB issued

authoritative guidance to defer the effective date for those aspects of the guidance relating to the presentation of

reclassification adjustments out of accumulated other comprehensive income by component. The guidance

became effective for the Company in the first quarter of fiscal year 2013 and has been retrospectively applied for

the fiscal year ended September 28, 2012. The adoption of this guidance did not have a material impact on the

Company’s financial position, results of operations or cash flows.

In September 2011, the FASB issued authoritative guidance which amends the process of testing goodwill

for impairment. The guidance permits an entity to first assess qualitative factors to determine whether the

existence of events or circumstances leads to a determination that it is more likely than not (defined as having a

likelihood of more than fifty percent) that the fair value of a reporting unit is less than its carrying amount. If an

entity determines it is not more likely than not that the fair value of a reporting unit is less than its carrying

amount, performing the traditional two-step goodwill impairment test is unnecessary. If an entity concludes

otherwise, it would be required to perform the first step of the two-step goodwill impairment test. If the carrying

amount of the reporting unit exceeds its fair value, then the entity is required to perform the second step of the

goodwill impairment test. However, an entity has the option to bypass the qualitative assessment in any period

and proceed directly to step one of the impairment test. The guidance became effective for the Company in the

first quarter of fiscal year 2013. The adoption of this guidance did not have a material impact on the Company’s

financial position, results of operations or cash flows.

In July 2012, the FASB issued authoritative guidance which amends the process of testing indefinite-lived

intangible assets for impairment. This guidance permits an entity to first assess qualitative factors to determine

whether the existence of events or circumstances leads to a determination that it is more likely than not (defined

as having a likelihood of more than fifty percent) that the indefinite-lived intangible asset is impaired. If an entity

determines it is not more likely than not that the indefinite-lived intangible asset is impaired, the entity will have

an option not to calculate the fair value of an indefinite-lived asset annually. The guidance became effective for

the Company in the first quarter of fiscal year 2013. The adoption of this guidance did not have a material impact

on the Company’s financial position, results of operations or cash flows.

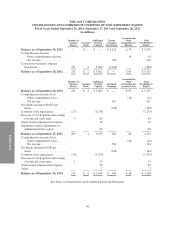

In February 2013, the FASB issued authoritative guidance which expands the disclosure requirements for

amounts reclassified out of accumulated other comprehensive income (“AOCI”). The guidance requires an entity

to provide information about the amounts reclassified out of AOCI by component and present, either on the face

of the income statement or in the notes to financial statements, significant amounts reclassified out of AOCI by

the respective line items of net income but only if the amount reclassified is required under GAAP to be

reclassified to net income in its entirety in the same reporting period. For other amounts, an entity is required to

cross-reference to other disclosures required under GAAP that provide additional detail about those amounts.

This guidance does not change the current requirements for reporting net income or other comprehensive income

in the financial statements. The guidance became effective for the Company in the first quarter of fiscal year

2014. The adoption of this guidance did not have a significant impact on the Company’s Consolidated and

Combined Financial Statements, as any reclassifications out of AOCI were immaterial.

In May 2014, the FASB issued authoritative guidance which sets forth a single comprehensive model for

entities to use in accounting for revenue arising from contracts with customers. The guidance is effective for

annual reporting periods (including interim reporting periods within those periods) beginning after December 15,

2016 and early adoption is not permitted. Companies may use either a full retrospective or a modified

retrospective approach to adopt this guidance. The Company is currently evaluating the impact of this guidance.

77