Singapore Airlines 2010 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2010 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

ANNUAL REPORT 2009/10

95

2 Summary of Significant Accounting Policies (continued)

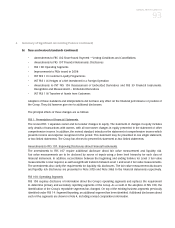

(b) New and revised standards (continued)

The management expects that the adoption of the above pronouncements will have no material impact to the

financial statements in the period of initial application except for the following:

Revised FRS 24: Related Party Disclosures

The revised FRS 24 expands the definition of a related party and would treat two entities as related to each other

whenever a person (or a close member of that person’s family) or a third party entity has control or joint control over

the entity, or has significant influence over the entity. The Group is currently determining the impact of the expanded

definition has on the disclosure of related party transactions. As this is a disclosure standard, it will have no impact

on the financial position or financial performance of the Group when implemented in 2011.

Revised FRS 103: Business Combinations and Amendments to FRS 27: Consolidated and Separate Financial Statements

The revised FRS 103 introduces a number of changes in the accounting for business combinations occurring after

1 July 2009. These changes will impact the amount of goodwill recognised, the reported results in the period that an

acquisition occurs, and future reported results. The Amendments to FRS 27 require that a change in the ownership

interest of a subsidiary company (without loss of control) is accounted for as an equity transaction. Therefore, such

transactions will no longer give rise to goodwill, nor will they give rise to a gain or loss. Furthermore, the amended

standard changes the accounting for losses incurred by the subsidiary company as well as the loss of control of

a subsidiary company. Other consequential amendments were made to FRS 7 Statement of Cash Flows, FRS 12

Income Taxes, FRS 21 The Effects of Changes in Foreign Exchange Rates, FRS 28 Investments in Associates and

FRS 31 Interests in Joint Ventures. The changes from revised FRS 103 and Amendments to FRS 27 will affect future

acquisitions or loss of control and transactions with minority interests. The standards may be early applied. However,

the Group does not intend to early adopt.

(c) Basis of consolidation

The consolidated financial statements comprise the separate financial statements of the Company and its subsidiary

companies as at the end of the reporting period. The financial statements of the subsidiary companies used in the

preparation of the consolidated financial statements are prepared for the same reporting date as the Company.

Consistent accounting policies are applied for like transactions and events in similar circumstances. A list of the

Group’s subsidiary companies is shown in Note 22 to the financial statements.

All intra-group balances, transactions, income and expenses and profits and losses resulting from intra-group

transactions are eliminated in full.

Acquisitions of subsidiary companies are accounted for using the purchase method. Identifiable assets acquired and

liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the

acquisition date. Adjustments to those fair values relating to previously held interests are treated as a revaluation and

recognised in equity. Any excess of the cost of the business combination over the Group’s share in the net fair value

of the acquired subsidiary company’s identifiable assets, liabilities and contingent liabilities is recorded as goodwill

on the statement of financial position. The accounting policy for goodwill is set out in Note 2(e)(i). Any excess of the

Group’s share in the net fair value of the acquired subsidiary company’s identifiable assets, liabilities and contingent

liabilities over the cost of the business combination is recognised in the profit and loss account on the date of acquisition.