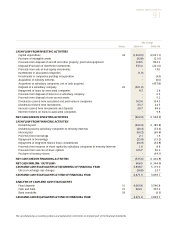

Singapore Airlines 2010 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2010 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

ANNUAL REPORT 2009/10

101

2 Summary of Significant Accounting Policies (continued)

(i) Investment properties (continued)

Investment properties are derecognised when either they have been disposed of or when the investment property is

permanently withdrawn from use and no future economic benefit is expected from its disposal. Any gains or losses

on the retirement or disposal of an investment property are recognised in the profit and loss account in the year of

retirement or disposal.

For a transfer from owner occupied property to investment property, the property is accounted for in accordance

with the accounting policy for property, plant and equipment set out in Note 2(g) up to the date of change in use.

(j) Leases

The determination of whether an arrangement is, or contains a lease is based on the substance of the arrangement

at inception date: whether fulfilment of the arrangement is dependent on the use of a specific asset or assets or the

arrangement conveys a right to use the asset. For arrangements entered into prior to 1 January 2005, the date of

inception is deemed to be 1 January 2005 in accordance with the transitional requirements of INT FRS 104.

(i) Finance lease – as lessee

Finance leases, which transfer to the Group substantially all the risks and benefits incidental to ownership of the

leased asset, are capitalised at the inception of the lease at the fair value of the leased asset or, if lower, at the

present value of the minimum lease payments. Any initial direct costs are also added to the amount capitalised.

Lease payments are apportioned between finance charges and reduction of the lease liability so as to achieve a

constant rate of interest on the remaining balance of the liability. Finance charges are charged directly against

the profit and loss account.

For sale and finance leaseback, differences between sales proceeds and net book values are taken to the

statement of financial position as deferred gain on sale and leaseback transactions, included under deferred

account and amortised over the minimum lease terms.

Major improvements and modifications to leased aircraft due to operational requirements are capitalised and

depreciated over the average expected life between major overhauls (estimated to be 4 to 6 years).

(ii) Operating lease – as lessee

Leases where the lessor effectively retains substantially all the risks and benefits of ownership of the leased

assets are classified as operating leases. Operating lease payments are recognised as an expense in the profit

and loss account on a straight-line basis over the lease term. The aggregate benefit of incentives provided by

the lessor is recognised as a reduction of rental expense over the lease term on a straight-line basis.

Gains or losses arising from sale and operating leaseback of aircraft are determined based on fair values.

Differences between sales proceeds and fair values are taken to the statement of financial position as deferred

gain on sale and leaseback transactions, included under deferred account and amortised over the minimum

lease terms.