Kroger 2014 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2014 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142

|

|

A-69

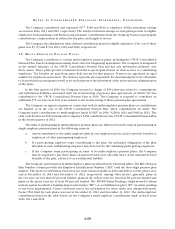

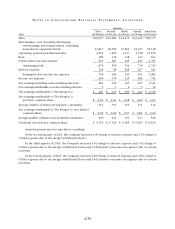

NO T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S , CO N T I N U E D

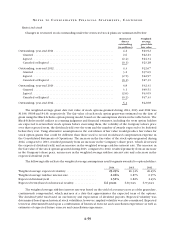

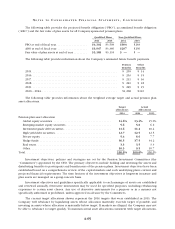

The Company contributed and expensed $177, $148 and $140 to employee 401(k) retirement savings

accounts in 2014, 2013 and 2012, respectively. The 401(k) retirement savings account plans provide to eligible

employees both matching contributions and automatic contributions from the Company based on participant

contributions, compensation as defined by the plan, and length of service.

The Company also administers other defined contribution plans for eligible employees. The cost of these

plans was $5, $5 and $7 for 2014, 2013 and 2012, respectively.

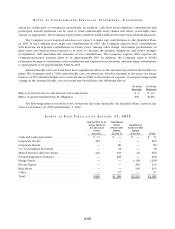

1 6 . M U L T I - E M P L O Y E R P E N S I O N P L A N S

The Company contributes to various multi-employer pension plans, including the UFCW Consolidated

Pension Plan, based on obligations arising from collective bargaining agreements. The Company is designated

as the named fiduciary of the UFCW Consolidated Pension Plan and has sole investment authority over

these assets. These plans provide retirement benefits to participants based on their service to contributing

employers. The benefits are paid from assets held in trust for that purpose. Trustees are appointed in equal

number by employers and unions. The trustees typically are responsible for determining the level of benefits

to be provided to participants as well as for such matters as the investment of the assets and the administration

of the plans.

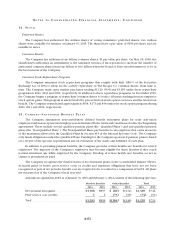

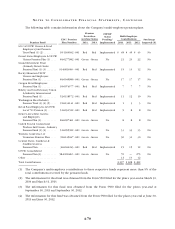

In the first quarter of 2014, the Company incurred a charge of $56 (after-tax) related to commitments

and withdrawal liabilities associated with the restructuring of pension plan agreements, of which $15 was

contributed to the UFCW Consolidated Pension Plan in 2014. The Company is required to contribute an

additional $75 over the next four years related to the restructuring of these pension plan agreements.

The Company recognizes expense in connection with its multi-employer pension plans as contributions

are funded, or in the case of the UFCW Consolidated Pension Plan, when commitments are made. The

Company made contributions to multi-employer funds of $297 in 2014, $228 in 2013 and $492 in 2012. The

cash contribution for 2012 includes the Company’s $258 contribution to the UFCW Consolidated Pension Plan

in the fourth quarter of 2012.

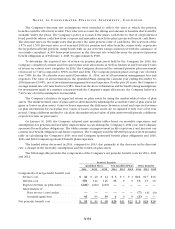

The risks of participating in multi-employer pension plans are different from the risks of participating in

single-employer pension plans in the following respects:

a. Assets contributed to the multi-employer plan by one employer may be used to provide benefits to

employees of other participating employers.

b. If a participating employer stops contributing to the plan, the unfunded obligations of the plan

allocable to such withdrawing employer may be borne by the remaining participating employers.

c. If the Company stops participating in some of its multi-employer pension plans, the Company

may be required to pay those plans an amount based on its allocable share of the unfunded vested

benefits of the plan, referred to as a withdrawal liability.

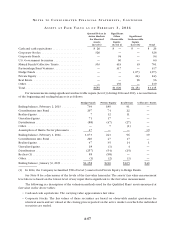

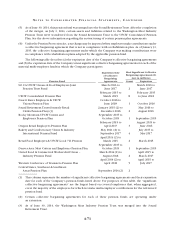

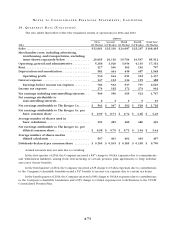

The Company’s participation in multi-employer plans is outlined in the following tables. The EIN / Pension

Plan Number column provides the Employer Identification Number (“EIN”) and the three-digit pension plan

number. The most recent Pension Protection Act Zone Status available in 2014 and 2013 is for the plan’s year-

end at December 31, 2013 and December 31, 2012, respectively. Among other factors, generally, plans in

the red zone are less than 65 percent funded, plans in the yellow zone are less than 80 percent funded and

plans in the green zone are at least 80 percent funded. The FIP/RP Status Pending / Implemented Column

indicates plans for which a funding improvement plan (“FIP”) or a rehabilitation plan (“RP”) is either pending

or has been implemented. Unless otherwise noted, the information for these tables was obtained from the

Forms 5500 filed for each plan’s year-end at December 31, 2013 and December 31, 2012. The multi-employer

contributions listed in the table below are the Company’s multi-employer contributions made in fiscal years

2014, 2013 and 2012.