Kroger 2014 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2014 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

|

|

A-64

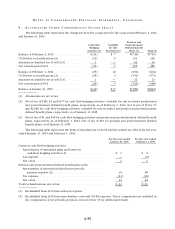

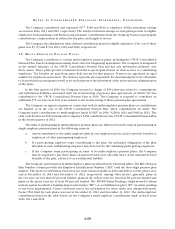

NO T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S , CO N T I N U E D

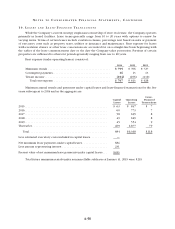

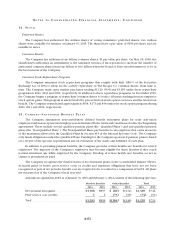

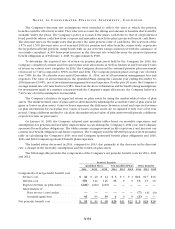

The Company’s discount rate assumptions were intended to reflect the rates at which the pension

benefits could be effectively settled. They take into account the timing and amount of benefits that would be

available under the plans. The Company’s policy is to match the plan’s cash flows to that of a hypothetical

bond portfolio whose cash flow from coupons and maturities match the plan’s projected benefit cash flows.

The discount rates are the single rates that produce the same present value of cash flows. The selection of the

3.87% and 3.74% discount rates as of year-end 2014 for pension and other benefits, respectively, represents

the hypothetical bond portfolio using bonds with an AA or better rating constructed with the assistance of

an outside consultant. A 100 basis point increase in the discount rate would decrease the projected pension

benefit obligation as of February 1, 2015, by approximately $500.

To determine the expected rate of return on pension plan assets held by the Company for 2014, the

Company considered current and forecasted plan asset allocations as well as historical and forecasted rates

of return on various asset categories. In 2014, the Company decreased the assumed pension plan investment

return rate to 7.44% compared to 8.50% in 2013 and 2012. The Company pension plan’s average rate of return

was 7.58% for the 10 calendar years ended December 31, 2014, net of all investment management fees and

expenses. The value of all investments in the Qualified Plans during the calendar year ending December 31,

2014 increased 5.65%, net of investment management fees and expenses. For the past 20 years, the Company’s

average annual rate of return has been 9.58%. Based on the above information and forward looking assumptions

for investments made in a manner consistent with the Company’s target allocations, the Company believes a

7.44% rate of return assumption is reasonable.

The Company calculates its expected return on plan assets by using the market-related value of plan

assets. The market-related value of plan assets is determined by adjusting the actual fair value of plan assets for

gains or losses on plan assets. Gains or losses represent the difference between actual and expected returns

on plan investments for each plan year. Gains or losses on plan assets are recognized evenly over a five year

period. Using a different method to calculate the market-related value of plan assets would provide a different

expected return on plan assets.

On January 31, 2015, the Company adopted new mortality tables based on mortality experience and

assumptions for generational mortality improvement in calculating the Company’s 2014 year end Company

sponsored benefit plans obligations. The tables assume an improvement in life expectancy and increase our

current year benefit obligation and future expenses. The Company used the RP-2000 projected 2021 mortality

table in calculating the Company’s 2013 year end Company sponsored benefit plans obligations and 2014,

2013 and 2012 Company-sponsored benefit plans expenses.

The funded status decreased in 2014, compared to 2013, due primarily to the decrease in the discount

rate, a change in the mortality assumptions and the return on plan assets.

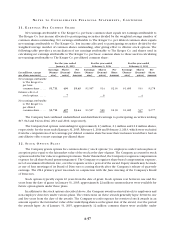

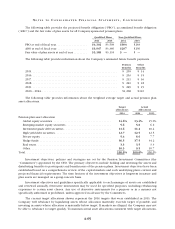

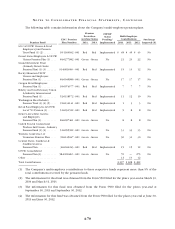

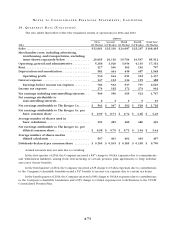

The following table provides the components of the Company’s net periodic benefit costs for 2014, 2013

and 2012:

Pension Benefits

Qualified Plans Non-Qualified Plans Other Benefits

2014 2013 2012 2014 2013 2012 2014 2013 2012

Components of net periodic benefit cost:

Service cost. . . . . . . . . . . . . . . . . . . . . . . . . $ 48 $ 40 $ 44 $ 3 $ 3 $ 3 $11 $17 $16

Interest cost . . . . . . . . . . . . . . . . . . . . . . . . 169 144 146 13 9 9 13 15 16

Expected return on plan assets. . . . . . . . . . (228) (224) (210) — — — — — —

Amortization of:

Prior service cost (credit) . . . . . . . . . . . — — — — — — (7) (4) (4)

Actuarial (gain) loss . . . . . . . . . . . . . . . . 46 93 88 4 9 9 (8) — —

Net periodic benefit cost . . . . . . . . . . . . . . . . . $ 35 $ 53 $ 68 $20 $21 $21 $ 9 $28 $28