Foot Locker 2013 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2013 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

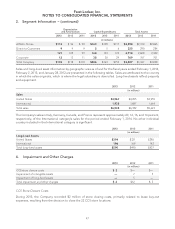

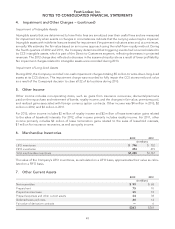

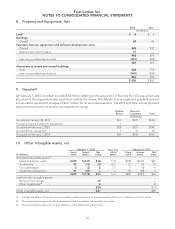

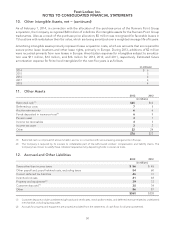

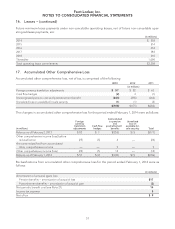

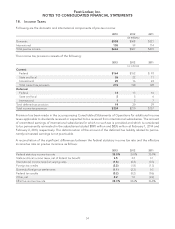

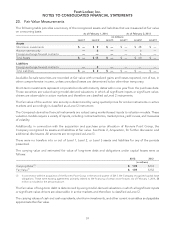

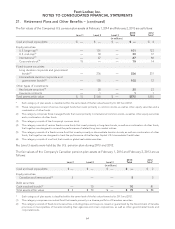

Foot Locker, Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

18. Income Taxes − (continued)

Settlements could increase earnings in an amount ranging from $0 to $5 million based on current estimates.

Audit outcomes and the timing of audit settlements are subject to significant uncertainty. Although manage-

ment believes that adequate provision has been made for such issues, the ultimate resolution could have an

adverse effect on the earnings of the Company. Conversely, if these issues are resolved favorably in the future,

the related provision would be reduced, generating a positive effect on earnings. Due to the uncertainty of

amounts and in accordance with its accounting policies, the Company has not recorded any potential impact

of these settlements.

19. Financial Instruments and Risk Management

The Company operates internationally and utilizes certain derivative financial instruments to mitigate its foreign

currency exposures, primarily related to third-party and intercompany forecasted transactions. As a result of the

use of derivative instruments, the Company is exposed to the risk that counterparties will fail to meet their

contractual obligations. To mitigate this counterparty credit risk, the Company has a practice of entering into

contracts only with major financial institutions selected based upon their credit ratings and other financial

factors. The Company monitors the creditworthiness of counterparties throughout the duration of the deriva-

tive instrument. Additional information is contained within Note 20, Fair Value Measurements.

Derivative Holdings Designated as Hedges

For a derivative to qualify as a hedge at inception and throughout the hedged period, the Company formally

documents the nature of the hedged items and the relationships between the hedging instruments and the

hedged items, as well as its risk-management objectives, strategies for undertaking the various hedge transac-

tions, and the methods of assessing hedge effectiveness and ineffectiveness. In addition, for hedges of

forecasted transactions, the significant characteristics and expected terms of a forecasted transaction must be

specifically identified, and it must be probable that each forecasted transaction would occur. If it were deemed

probable that the forecasted transaction would not occur, the gain or loss on the derivative instrument would

be recognized in earnings immediately. No such gains or losses were recognized in earnings for any of the

periods presented. Derivative financial instruments qualifying for hedge accounting must maintain a specified

level of effectiveness between the hedging instrument and the item being hedged, both at inception and

throughout the hedged period, which management evaluates periodically.

The primary currencies to which the Company is exposed are the euro, British pound, Canadian dollar, and

Australian dollar. For option and foreign exchange forward contracts designated as cash flow hedges of the

purchase of inventory, the effective portion of gains and losses is deferred as a component of Accumulated

Other Comprehensive Loss (‘‘AOCL’’) and is recognized as a component of cost of sales when the related

inventory is sold. The amount reclassified to cost of sales related to such contracts was not significant for any of

the periods presented. The effective portion of gains or losses associated with other forward contracts is

deferred as a component of AOCL until the underlying transaction is reported in earnings. The ineffective

portion of gains and losses related to cash flow hedges recorded to earnings was also not significant for any of

the periods presented. When using a forward contract as a hedging instrument, the Company excludes the

time value of the contract from the assessment of effectiveness. For all years presented, the Company had not

hedged forecasted transactions for more than the next twelve months, and the Company expects all derivative-

related amounts reported in AOCL to be reclassified to earnings within twelve months. During 2013, the net

change in the fair value of the foreign exchange derivative financial instruments designated as cash flow hedges

of the purchase of inventory resulted in a loss of $5 million and therefore increased AOCL. At February 1, 2014

there was a $2 million loss included in AOCL.

The notional value of the contracts outstanding at February 1, 2014 was $70 million and these contracts extend

through January 2015.

57