Albertsons 2004 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2004 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

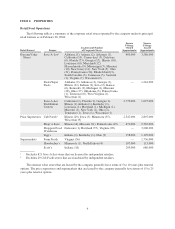

sales to extreme value stores licensed by the company. Food distribution operations include results of sales to

affiliated food stores, mass merchants and other customers, and other logistics arrangements. Management

utilizes more than one measurement and multiple views of data to assess segment performance and to allocate

resources to the segments. However, the dominant measurements are consistent with the consolidated financial

statements. The financial information concerning the company’s operations by reportable segment for the years

ended February 28, 2004, February 22, 2003 and February 23, 2002 is contained on page F-5.

Retail Food Operations

Overview.AtFebruary 28, 2004, the company conducted its retail food operations through a total of

1,483 retail stores, including 821 licensed extreme value stores. Its principal retail food formats include extreme

value stores, regional price superstores and regional supermarkets. These diverse formats enable the company to

operate in a variety of markets under widely differing competitive circumstances. Based on revenues, the

company was the 11th largest grocery retailer in the United States as of February 28, 2004. In fiscal 2005, the

company anticipates opening approximately 110 to 140 new extreme value stores and eight to 10 regional banner

stores and continuing its store remodeling program.

Extreme Value Stores. The company operates extreme value stores primarily under the Save-A-Lot

banner. Save-A-Lot holds the number one market position, based on revenues, in the extreme value grocery-

retailing sector. Save-A-Lot food stores typically are approximately 15,000 square feet in size, and stock

approximately 1,250 high volume food items generally in a single size for each product sold. At a Save-A-Lot

store, the majority of the products offered for sale are custom branded products. The specifications for the Save-

A-Lot custom branded product emphasize quality and characteristics that the company believes are comparable

to national brands. The company’s attention to the packaging of Save-A-Lot products has resulted in the

company registering a number of its custom labels.

After the company’s fiscal 2003 acquisition of a small dollar store general merchandise operator, Deal$

Nothing Over A Dollar (“Deals”), the company started testing several new prototypes of an extreme value

combination store, offering both food and dollar-priced general merchandise. During fiscal 2004, the company

converted or opened 166 combination stores.

At fiscal year end, there were 1,225 extreme value stores located in 37 states, of which 821 were licensed.

These stores are supplied from 16 dedicated distribution centers.

Price Superstores. The company’s price superstores hold the number one, two or three market position in

most of their markets. The price superstore focus is on providing every day low prices and product selection

across all departments. Most of the company’s price superstores offer traditional dry grocery departments, along

with strong perishable departments and pharmacies. Price superstores carry over 45,000 items and generally

range in size from 45,000 to 100,000 square feet with an average size of approximately 64,000 square feet.

At fiscal year end, the company owned and operated 199 price superstores under the Cub Foods, Shop ’n

Save, Shoppers Food Warehouse and bigg’s banners in 12 states; an additional 29 stores were franchised to

independent retailers under the Cub Foods banner. In-store pharmacies are operated in 176 of the price

superstores.

The owned Cub Food stores operate primarily in the Minneapolis/St. Paul and Chicago markets; Shop ’n

Save operates primarily in the St. Louis and Pittsburgh markets; Shoppers Food Warehouse operates in the

Washington D.C. and Baltimore markets; and bigg’s operates primarily in the Cincinnati market.

Supermarkets. The company’s traditional supermarkets hold the number one or two market positions in

their principal markets. This format combines a grocery store that offers traditional dry grocery and fresh food

departments, and a variety of specialty departments that may include floral, seafood, expanded health and beauty

care, video rental, cosmetics, photo finishing, delicatessen, bakery, as well as an in-store bank and a traditional

3