Albertsons 2004 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2004 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

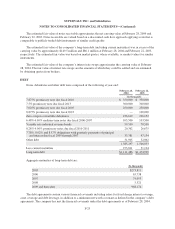

SUPERVALU INC. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

The estimated fair value of notes receivable approximates the net carrying value at February 28, 2004 and

February 22, 2003. Notes receivable are valued based on a discounted cash flow approach applying a rate that is

comparable to publicly traded debt instruments of similar credit quality.

The estimated fair value of the company’s long-term debt (including current maturities) was in excess of the

carrying value by approximately $149.5 million and $86.1 million at February 28, 2004 and February 22, 2003,

respectively. The estimated fair value was based on market quotes, where available, or market values for similar

instruments.

The estimated fair value of the company’s interest rate swaps approximates the carrying value at February

28, 2004. The fair value of interest rate swaps are the amounts at which they could be settled and are estimated

by obtaining quotes from brokers.

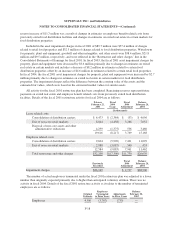

DEBT

Notes, debentures and other debt were composed of the following at year-end:

February 28,

2004

February 22,

2003

(In thousands)

7.875% promissory note due fiscal 2010 $ 350,000 $ 350,000

7.5% promissory note due fiscal 2013 300,000 300,000

7.625% promissory note due fiscal 2005 250,000 250,000

8.875% promissory note due fiscal 2023 — 100,000

Zero-coupon convertible debentures 236,619 226,152

6.48%-6.69% medium-term notes due fiscal 2006-2007 103,500 103,500

Variable rate industrial revenue bonds 59,530 70,530

8.28%-9.96% promissory notes due fiscal 2010-2011 20,362 26,675

7.78%, 8.02% and 8.57% obligations with quarterly payments of principal

and interest due fiscal 2005 through 2007 33,381 47,134

Other debt 31,905 32,062

1,385,297 1,506,053

Less current maturities 273,811 31,124

Long-term debt $1,111,486 $1,474,929

Aggregate maturities of long-term debt are:

(In thousands)

2005 $273,811

2006 63,738

2007 74,053

2008 5,521

2009 and thereafter 968,174

The debt agreements contain various financial covenants including ratios for fixed charge interest coverage,

asset coverage and debt leverage, in addition to a minimum net worth covenant as defined in the company’s debt

agreements. The company has met the financial covenants under the debt agreements as of February 28, 2004.

F-23