US Airways 2004 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2004 US Airways annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

Table of Contents

AMERICA WEST AIRLINES, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — CONTINUED

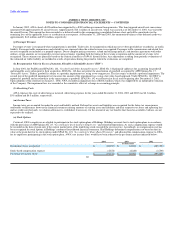

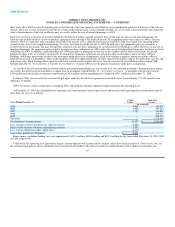

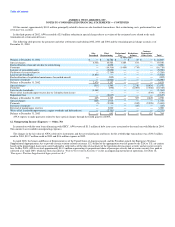

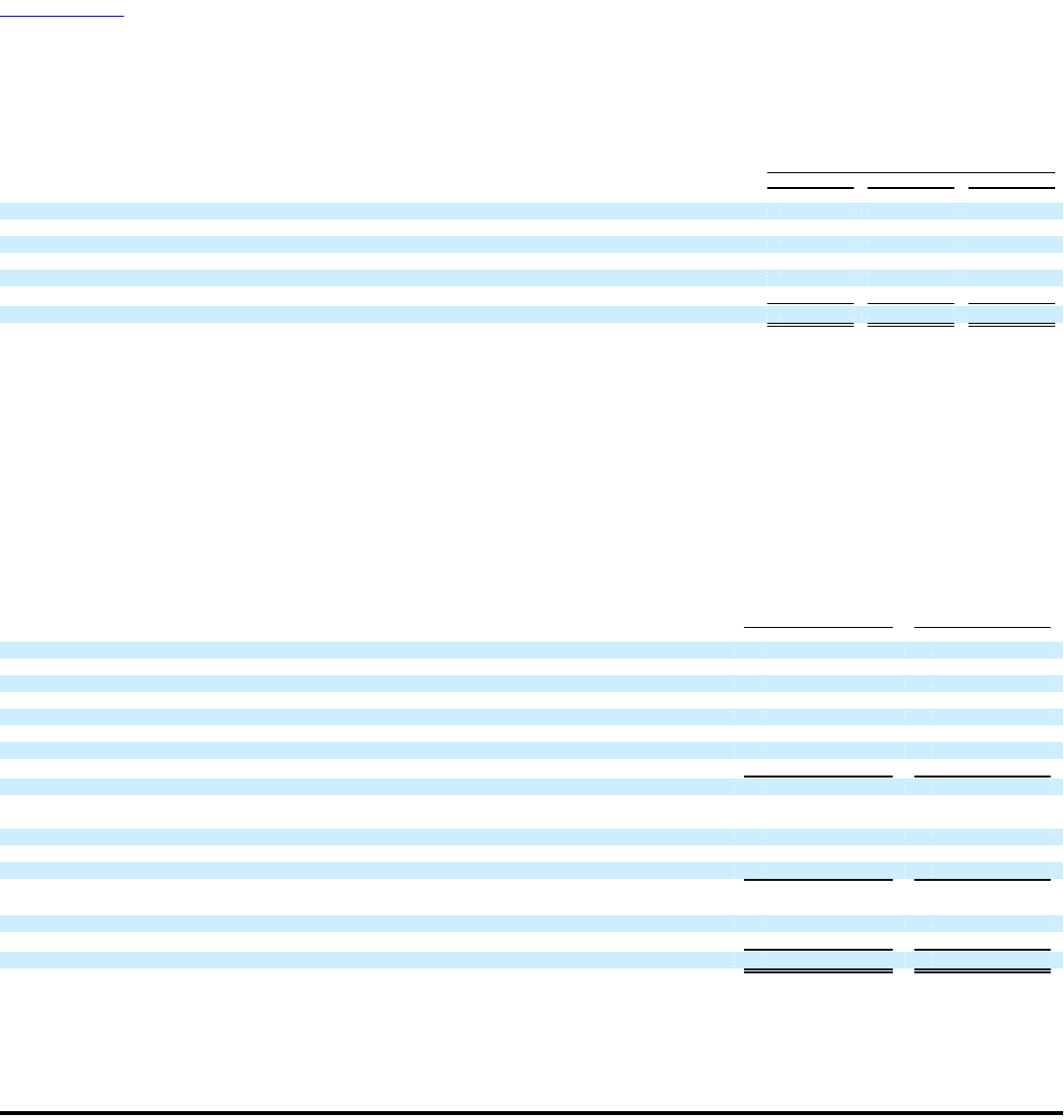

Income tax expense (benefit) differs from amounts computed at the federal statutory income tax rate as follows:

Year Ended December 31,

2004 2003 2002

(in thousands)

Income tax expense (benefit) at the federal statutory income tax rate $ (29,832) $ 21,490 $ (74,207)

State income tax expense (benefit), net of federal income tax expense (benefit) (3,057) 2,532 (7,920)

State rate change — (3,229) —

Change in valuation allowance 31,036 (17,532) 44,461

Expired tax credits — — 7,988

Other, net 1,876 (3,147) (866)

Total $ 23 $ 114 $ (30,544)

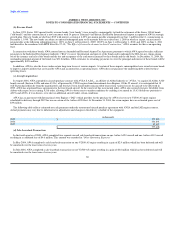

As of December 31, 2004, AWA has available net operating loss carryforwards ("NOLs") and tax credit carryforwards for federal income tax purposes of

approximately $447.6 million and $1.1 million, respectively. The NOLs expire during the years 2007 through 2024 while approximately $0.2 million of the

tax credit carryforwards will expire in 2005 and 2006. AWA also had capital loss carryforwards for federal income tax purposes of approximately

$1.4 million which expire in 2009. However, such carryforwards are not available to offset federal (and in certain circumstances, state) alternative minimum

taxable income. Further, as a result of a statutory "ownership change" (as defined for purposes of Section 382 of the Internal Revenue Code) that occurred as a

result of AWA's reorganization in 1994, AWA's ability to utilize its NOLs and tax credit carryforwards may be restricted.

In September 2003, Holdings filed its 2002 consolidated income tax return with the IRS, which included a claim to carryback losses incurred in 2002 to the

tax years 1999 and 2000. This resulted in a refund of approximately $3.1 million, of which substantially all was received in the fourth quarter of 2003.

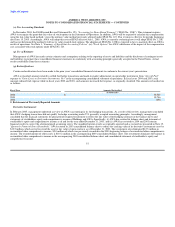

Composition of Deferred Tax Items:

Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting

purposes and the amounts used for income tax purposes. As of December 31, the significant components of AWA's deferred tax assets and liabilities are a

result of the temporary differences related to the items described as follows:

2004 2003

(in thousands)

Deferred tax assets:

Net operating loss carryforwards $ 183,058 $ 126,220

Aircraft leases 13,585 17,347

Vacation accrual 13,407 11,948

Frequent flyer accrual 6,592 5,958

Restructuring and other reserves 3,626 3,858

Tax credit carryforwards 1,112 1,112

Other 3,144 2,740

Gross deferred tax assets 224,524 169,183

Deferred tax liabilities:

Accelerated depreciation and amortization (95,365) (70,534)

Partnership losses (1,421) (1,420)

Other (254) (781)

Gross deferred tax liabilities (97,040) (72,735)

Net deferred tax assets before valuation allowance 127,484 96,448

Less valuation allowance (127,484) (96,448)

Net deferred liability — —

SFAS No. 109, "Accounting for Income Taxes," requires that a valuation allowance be established when it is "more likely than not" that all or a portion of

deferred tax assets will not be realized. A review of all available positive and negative evidence needs to be considered, including AWA's performance, the

market environment in which AWA operates, forecasts of future profitability, the utilization of past tax credits, length of carryforward periods and similar

factors. SFAS No. 109 further states that it is difficult to conclude that a valuation allowance is

90