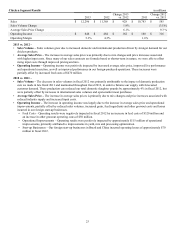

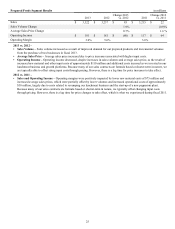

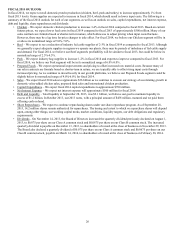

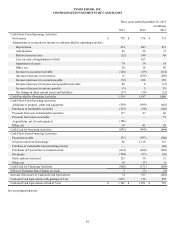

Tyson Foods 2013 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2013 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

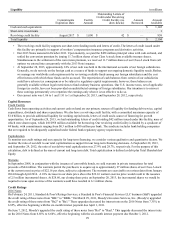

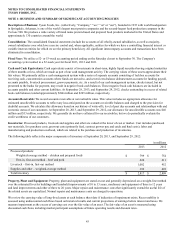

33

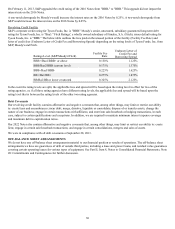

Description Judgments and Uncertainties Effect if Actual Results Differ From

Assumptions

Accrued self-insurance

We are self insured for certain losses

related to health and welfare, workers’

compensation, auto liability and general

liability claims.

We use an independent third-party actuary

to assist in determining our self-insurance

liability. We and the actuary consider a

number of factors when estimating our

self-insurance liability, including claims

experience, demographic factors, severity

factors and other actuarial assumptions.

We periodically review our estimates and

assumptions with our third-party actuary

to assist us in determining the adequacy of

our self-insurance liability. Our policy is

to maintain an accrual within the central

to high point of the actuarial range.

Our self-insurance liability contains

uncertainties due to assumptions required

and judgment used.

Costs to settle our obligations, including

legal and healthcare costs, could increase

or decrease causing estimates of our self-

insurance liability to change.

Incident rates, including frequency and

severity, could increase or decrease

causing estimates in our self-insurance

liability to change.

We have not made any material changes

in the accounting methodology used to

establish our self-insurance liability

during the past three fiscal years.

We do not believe there is a reasonable

likelihood there will be a material change

in the estimates or assumptions used to

calculate our self-insurance liability.

However, if actual results are not

consistent with our estimates or

assumptions, we may be exposed to gains

or losses that could be material.

A 10% increase in the actuarial estimate at

September 28, 2013, would result in an

increase in the amount we recorded for

our self-insurance liability of

approximately $11 million. A 10%

decrease in the actuarial estimate at

September 28, 2013, would result in a

decrease in the amount we recorded for

our self-insurance liability of

approximately $17 million.

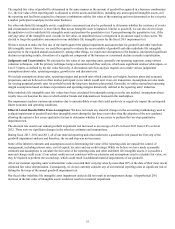

Income taxes

We estimate total income tax expense

based on statutory tax rates and tax

planning opportunities available to us in

various jurisdictions in which we earn

income.

Federal income tax includes an estimate

for taxes on earnings of foreign

subsidiaries expected to be taxable upon

remittance to the United States, except for

earnings considered to be indefinitely

invested in the foreign subsidiary.

Deferred income taxes are recognized for

the future tax effects of temporary

differences between financial and income

tax reporting using tax rates in effect for

the years in which the differences are

expected to reverse.

Valuation allowances are recorded when it

is likely a tax benefit will not be realized

for a deferred tax asset.

We record unrecognized tax benefit

liabilities for known or anticipated tax

issues based on our analysis of whether,

and the extent to which, additional taxes

will be due.

Changes in tax laws and rates could affect

recorded deferred tax assets and liabilities

in the future.

Changes in projected future earnings

could affect the recorded valuation

allowances in the future.

Our calculations related to income taxes

contain uncertainties due to judgment

used to calculate tax liabilities in the

application of complex tax regulations

across the tax jurisdictions where we

operate.

Our analysis of unrecognized tax benefits

contains uncertainties based on judgment

used to apply the more likely than not

recognition and measurement thresholds.

We do not believe there is a reasonable

likelihood there will be a material change

in the tax related balances or valuation

allowances. However, due to the

complexity of some of these uncertainties,

the ultimate resolution may result in a

payment that is materially different from

the current estimate of the tax liabilities.

To the extent we prevail in matters for

which unrecognized tax benefit liabilities

have been established, or are required to

pay amounts in excess of our recorded

unrecognized tax benefit liabilities, our

effective tax rate in a given financial

statement period could be materially

affected. An unfavorable tax settlement

would require use of our cash and

generally result in an increase in our

effective tax rate in the period of

resolution. A favorable tax settlement

would generally be recognized as a

reduction in our effective tax rate in the

period of resolution.