Saks Fifth Avenue 2011 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2011 Saks Fifth Avenue annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

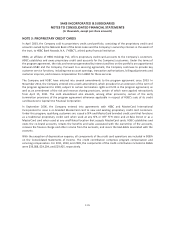

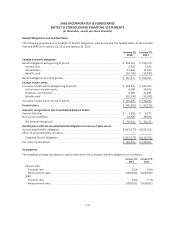

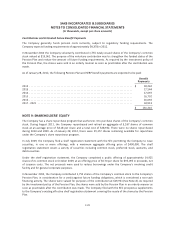

SAKS INCORPORATED & SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(In thousands, except per share amounts)

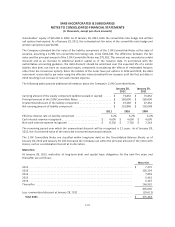

Authoritative accounting literature requires the allocation of convertible debt proceeds between the liability

component and the embedded conversion option (i.e., the equity component). The liability component of the

debt instrument is accreted to par value using the effective interest method over the remaining life of the debt.

The accretion is reported as a component of interest expense. The equity component is not subsequently

revalued as long as it continues to qualify for equity treatment. Upon issuance, the Company estimated the fair

value of the liability component of the 7.5% Convertible Notes, assuming a 13.0% non-convertible borrowing

rate, to be $97,994. The difference between the fair value and the principal amount of the 7.5% Convertible

Notes was $22,006. This amount was recorded as a debt discount and as an increase to additional paid-in

capital as of the issuance date. The discount is being accreted to interest expense over the 4.5 year period to

the maturity date of the notes in December 2013 resulting in an increase in non-cash interest expense.

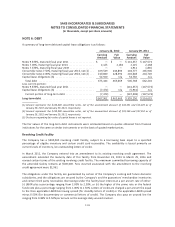

The following tables provide additional information about the Company’s 7.5% Convertible Notes.

January 28,

2012

January 29,

2011

Carrying amount of the equity component (additional paid-in capital) ..... $ 22,006 $ 22,006

Principal amount of the 7.5% Convertible Notes ....................... $ 120,000 $ 120,000

Unamortized discount of the liability component ...................... $ 10,451 $ 15,223

Net carrying amount of liability component .......................... $ 109,549 $ 104,777

2011 2010 2009

Effective interest rate on liability component ................. 12.9% 12.9% 12.9%

Cash interest expense recognized .......................... $ 9,000 $ 9,000 $ 6,100

Non-cash interest expense recognized ...................... $ 4,772 $ 4,207 $ 2,576

The remaining period over which the unamortized discount will be recognized is 1.8 years. As of January 28,

2012, the if-converted value of the notes exceeded its principal amount by $91,066.

The 7.5% Convertible Notes are classified within long-term debt on the Consolidated Balance Sheets as of

January 28, 2012 and January 29, 2011 because the Company can settle the principal amount of the notes with

shares, cash, or a combination thereof at its discretion.

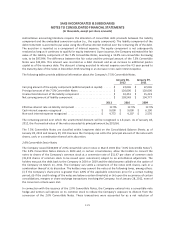

2.0% Convertible Senior Notes

The Company issued $230,000 of 2.0% convertible senior notes in March 2004 (the “2.0% Convertible Notes”).

The 2.0% Convertible Notes mature in 2024 and, in certain circumstances, allow the holders to convert the

notes to shares of the Company’s common stock at a conversion rate of $11.97 per share of common stock

(19,219 shares of common stock to be issued upon conversion) subject to an anti-dilution adjustment. The

holders may put the debt back to the Company in 2014 or 2019 and the debt became callable at the option of

the Company on March 21, 2011. The Company can settle a conversion of the notes with shares, cash or a

combination thereof at its discretion. The holders may convert the notes at the following times, among others:

(i) if the Company’s share price is greater than 120% of the applicable conversion price for a certain trading

period; (ii) if the credit ratings of the notes are below a certain threshold; or (iii) upon the occurrence of certain

consolidations, mergers or share exchange transactions involving the Company. As of January 28, 2012, none of

the conversion criteria were met.

In connection with the issuance of the 2.0% Convertible Notes, the Company entered into a convertible note

hedge and written call options on its common stock to reduce the Company’s exposure to dilution from the

conversion of the 2.0% Convertible Notes. These transactions were accounted for as a net reduction of

F-21