Saks Fifth Avenue 2011 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2011 Saks Fifth Avenue annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

In September of 2006, the Company entered into agreements with HSBC and MasterCard International

Incorporated to issue co-branded MasterCard cards to new and existing proprietary credit card customers.

Under this program, qualifying customers are issued an SFA and MasterCard co-branded credit card that

functions as a traditional proprietary credit card when used at any SFA or OFF 5TH store and at Saks Direct or as

a MasterCard card when used at any unaffiliated location that accepts MasterCard cards. HSBC establishes and

owns the co-brand accounts, retains the benefits associated with the ownership of the accounts, receives the

finance charge and other income from the accounts, and incurs the bad debts associated with the accounts.

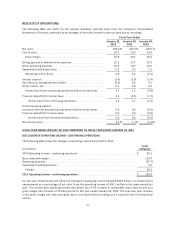

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The Company’s critical accounting policies and estimates are discussed in the notes to the consolidated financial

statements. Certain judgments and estimates utilized in implementing these accounting policies are likewise

discussed in each of the notes to the consolidated financial statements. The following discussion sets forth the

judgments and uncertainties affecting the application of these policies and estimates and the likelihood that

materially different amounts would be reported under varying conditions and assumptions.

REVENUE RECOGNITION

Revenue from the sale of merchandise at the Company’s retail stores is recognized at the time customers

provide a satisfactory form of payment and take delivery of the merchandise. Revenue from the sale of

merchandise from Saks Direct is recognized upon estimated receipt of merchandise by the customer. The

Company estimates the amount of goods that will be returned for a refund based on historical trends and

reduces sales and gross margin by that amount. Given that approximately 22% of merchandise sold is later

returned and that the vast majority of merchandise returns occur within a short time after the selling

transaction, the risk of the Company realizing a materially different amount for sales and gross margin than

reported in the consolidated financial statements is minimal.

Revenue associated with gift cards is recognized upon redemption by the customer. Breakage income

associated with unredeemed gift cards is recognized if the gift card is not subject to state escheatment laws

when the likelihood of customer redemption is determined to be remote.

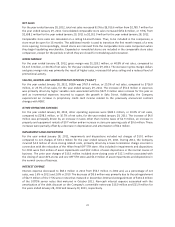

COST OF SALES AND INVENTORY VALUATION

Merchandise inventories are stated at the lower of cost or market, with cost being determined using the retail

first-in, first-out (“FIFO”) method. Under the retail inventory method, the valuation of inventories at cost and

the resulting gross margins are determined by applying a calculated cost-to-retail ratio to the retail value of

inventories. The cost of the inventory reflected on the consolidated balance sheet is decreased with a charge to

cost of sales contemporaneous with the lowering of the retail value of the inventory on the sales floor through

the use of markdowns. Hence, earnings are negatively impacted as the merchandise is being devalued with

markdowns prior to the sale of the merchandise. The areas requiring significant management judgment include

(1) setting the original retail value for the merchandise held for sale, (2) recognizing merchandise for which the

customer’s perception of value has declined and appropriately marking the retail value of the merchandise

down to the perceived value, and (3) estimating the shrinkage that has occurred through theft during the period

between physical inventory counts.

These judgments and estimates, coupled with the averaging processes within the retail method, can, under

certain circumstances, produce varying financial results. Factors that can lead to different financial results

include setting original retail prices for merchandise held for sale too high, failure to identify a decline in

perceived value of inventories and process the appropriate retail value markdowns, and overly optimistic or

overly conservative inventory shrinkage estimates. The Company believes it has the appropriate merchandise

valuation and pricing controls in place to minimize the risk that its inventory values would be materially under

or overvalued.

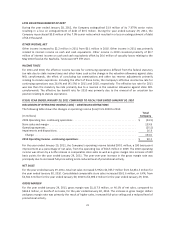

The Company regularly records a provision for estimated shrinkage, thereby reducing the carrying value of

merchandise inventory. A complete physical inventory of all of the Company’s stores and distribution facilities is

30