Saks Fifth Avenue 2011 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2011 Saks Fifth Avenue annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

CASH BALANCES AND LIQUIDITY

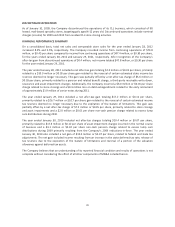

The Company’s primary sources of short-term liquidity are cash on hand and availability under its $500.0 million

revolving credit facility. The amount of cash on hand and borrowings under that facility are influenced by a

number of factors, including sales, inventory levels, vendor terms, the level of capital expenditures, cash

requirements related to financing instruments, and the Company’s tax payment obligations, among others. As

of January 28, 2012 and January 29, 2011, the Company maintained cash and cash equivalent balances of

$200.2 million and $197.9 million, respectively. Exclusive of $4.7 million and $7.9 million of store operating cash

as of January 28, 2012 and January 29, 2011, respectively, cash was invested primarily in money market funds,

demand deposits, and time deposits.

The primary needs for cash are to fund operations, acquire or construct new stores, renovate and expand

existing stores, provide working capital for new and existing stores, invest in technology and distribution centers

and service debt. The Company estimates capital expenditures for 2012 will be between $110 and $120 million,

net of tenant allowances and other proceeds. The Company anticipates that working capital requirements

related to existing stores, store renovations and capital expenditures will be funded through cash on hand, cash

provided by operations, and the revolving credit facility.

There are numerous general business and economic factors affecting the retail industry. These factors include

consumer confidence levels, intense competition, global economic conditions and financial market stability.

Significant changes in one or more of these factors could potentially have a material adverse impact on the

Company’s ability to generate sufficient cash flows to operate its business. The Company expects to be able to

manage its working capital and capital expenditure amounts so as to maintain sufficient levels of liquidity.

Depending upon its actual and anticipated sources and uses of liquidity, conditions in the capital markets and

other factors, the Company may from time to time consider the issuance of debt or other securities or other

possible capital market transactions for the purpose of raising capital which could be used to refinance current

indebtedness or for other corporate purposes.

CAPITAL STRUCTURE

The Company continuously evaluates its debt-to-capitalization ratio in light of business and economic trends,

interest rate levels, and the terms, conditions and availability of capital in the capital markets. As of January 28,

2012, the Company’s capital and financing structure was comprised of a revolving credit facility, senior

unsecured notes, convertible senior unsecured notes, and capital and operating leases. As of January 28, 2012,

total funded debt (including the equity component of the convertible notes) was $405.0 million, representing a

decrease of $144.3 million from the balance of $549.3 million at January 29, 2011. This decrease in debt was

primarily the result of the maturity of $141.6 million of the Company’s 9.875% senior notes and the redemption

of $1.9 million of the Company’s 7.375% senior notes and a net decrease in capital lease obligations of $0.8

million. Additionally, the Company’s debt-to-capitalization ratio decreased to 25.6% in 2011 from 32.9% in

2010.

Revolving Credit Facility

As of January 28, 2012, the Company maintained a $500.0 million revolving credit facility, which is subject to a

borrowing base equal to a specified percentage of eligible inventory and certain credit card receivables. As the

Company’s inventory levels fluctuate, these changes will, at times, cause the borrowing capacity to fall below

the stated $500.0 million maximum. In March 2011, the Company entered into an amendment to its existing

revolving credit agreement. The amendment extended the maturity date of the facility to March 2016 and

favorably revised certain terms of the existing facility, including, among other things, lower interest rates and

fees. The maximum borrowing capacity of the amended facility remains at $500.0 million. As of January 28,

2012, the Company had no direct borrowings under its revolving credit facility. Based on the inventory and

credit card receivable balances as of January 28, 2012, the Company had $471.5 million of availability under the

facility, after deducting outstanding letters of credit of $6.4 million.

26