Pizza Hut 1999 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 1999 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72

|

|

61

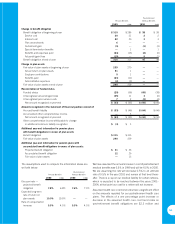

The 1997 financial data we reported above is materially consis-

tent with restaurant segment information previously reported by

PepsiCo. We made adjustments to these amounts primarily to

remove the impact of the restaurant distribution business previ-

ously included by PepsiCo in its restaurant segment, and to

include the investment in and our equity income of unconsoli-

dated affiliates within the international segment. We made this

change to align our reporting with the way we internally

review and make decisions regarding our interna-

tional business.

Commitments and Contingencies

Contingent Liabilities. We were directly or indi-

rectly contingently liable in the amounts of

$386 million and $327 million at year-end 1999 and 1998,

respectively, for certain lease assignments and guarantees. In

connection with these contingent liabilities, after the Spin-off

Date, we were required to maintain cash collateral balances at

certain institutions of approximately $30 million, which is

included in Other Assets in the accompanying Consolidated

Balance Sheet. At year-end 1999, $311 million represented

contingent liabilities to lessors as a result of assigning our inter-

est in and obligations under real estate leases as a condition to

the refranchising of Company restaurants. The $311 million

represented the present value of the minimum payments of the

assigned leases, excluding any renewal option periods, dis-

counted at our pre-tax cost of debt. On a nominal basis, the

contingent liability resulting from the assigned leases was

$485 million. The balance of the contingent liabilities primarily

reflected guarantees to support financial arrangements of cer-

tain unconsolidated affiliates and other restaurant franchisees.

Casualty Loss Programs and Estimates. To mitigate the

cost of our exposures for certain casualty losses as defined in

Note 5, we make annual decisions to either retain the risks of

loss up to certain per occurrence or maximum loss limits

negotiated with our insurance carriers or to fully insure those

risks. Since the Spin-off, we have elected to retain the risks

subject to insured limitations. In addition, we also purchased

insurance in 1998 to limit the cost of our retained risks for the

years 1994 to 1996.

Effective August 16, 1999, we made changes to our U.S. and

portions of our International property and casualty loss pro-

grams which we believe will reduce our annual property and

casualty costs. Under the new program, we bundled our risks

for casualty losses, property losses and various other insurable

risks into one risk pool with a single large retention limit. Based

on our historical casualty loss experience over the past ten

years, we believe that the combination of the annual risk of loss

that we retained and the lower insurance premium costs under

the new program should be less than the average total costs

incurred under the old program. However, since all of these

risks have been pooled and there are no per occurrence limits

for individual claims, it is possible that we may experience

increased volatility in property and casualty losses on a quarter

to quarter basis. This would occur if an individual large loss is

incurred either early in a program year or when the latest actu-

arial projection of losses for a program year is significantly below

our aggregate loss retention. A large loss is defined as a loss in

excess of $2 million which was our predominate per occurrence

casualty loss limit under our previous insurance program.

Under both our old and new programs, we have determined

our retained liabilities for casualty losses, including reported

and incurred but not reported claims, based on information

provided by our independent actuary. Effective August 16,

1999, property losses are also included in our actuary’s valua-

tion. Prior to that date, property losses were based on our

internal estimates.

We have our actuary perform valuations two times a year.

However, given the complexities of the Spin-off, we had only

one 1998 valuation, based on information through June 30,

1998, which we received and recognized in the fourth quarter

of that year. In the first and fourth quarters of 1999, we

received a valuation from the actuary based on information

through December 31, 1998 and June 30, 1999, respectively.

As a result, we have a timing difference in our actuarial adjust-

ments, from recognizing the entire 1998 adjustment in the

fourth quarter of 1998 to recognizing adjustment in both the

first quarter and fourth quarter of 1999. We expect that, begin-

ning in 2000, valuations will be received and required

adjustments will be made in the second and fourth quarters of

each year.

We have recorded favorable adjustments to our casualty loss

reserves of $30 million in 1999 ($21 million in the first quarter

and $9 million in the fourth quarter), $23 million in 1998 and

$18 million in 1997 primarily as a result of our independent

actuary’s changes in its estimated losses. The changes were

related to previously recorded casualty loss estimates deter-

mined by our independent actuary for both the current and

prior years in which we retained some risk of loss. The 1999

adjustments resulted primarily from improved loss trends

related to our 1998 casualty losses across all three of our U.S.

operating companies. We believe the favorable adjustments are

a direct result of our recent investments in safety and security

note 21